In our last article, we explored why payments matter when it comes to your company valuation. Now we’re going to dig into the details about how strategic buyers will evaluate your embedded payments. We’ll cover the baseline and standout metrics they want to see and how you should plan your embedded fintech approach to meet those expectations.

Invest in your payments proof points

“It’s a lot easier to sell a payments story when there’s actual revenue. Buyers want proof points—not just a narrative.”

You need to demonstrate that payments is not just a capability, but a proven monetization stream. What this means is showcasing real adoption within the install base and increasing penetration over time.

Real adoption means tracking payment volume over time. Showcase how it is trending. Dig into the cohorts over time.

Stop measuring payment penetration as a snapshot. Start measuring it as a cohort.

Most platforms look at payment penetration today and call it a day. But that number tells you almost nothing on its own. The real question is: what did your cohort from three years ago look like when they signed on, and how has that group grown since?

Cohort analysis shifts the conversation from “where are we now” to “are we actually getting better at this.” Are onboarding improvements moving the needle? Is a new pricing model driving faster adoption? Are targeted campaigns pulling more volume through the platform over time?

Track penetration by cohort, and you stop guessing. You start seeing exactly which levers work, and which ones are just noise.

Finally, you need to own your metrics up and down the P&L. It’s not only about total payment volume and penetration rate, it’s knowing your net take rate. You need to demonstrate real ownership over the net revenue line item.

Your Best-in-Class Payments & SaaS Structure

If you’re still debating how to structure your payments into your Vertical SaaS foundation, Brad is certain there’s a winning structure. You want to showcase both predictable revenue and a growth upside. That’s why this model wins:

Strong SaaS foundation

Payments revenue layered on top

“SaaS sells seats and workflows—but payments monetizes activity. The customer can grow, and you’re doing nothing, and still generating more revenue.”

This approach de-risks revenue, enhances valuation clarity, and it balances stability and expansion. It shows the most holistic view of your business.

If you’re an earlier stage company, you’ll require a heavier SaaS base. As you scale, you’ll likely need to meet a minimum SaaS floor to ensure buyer confidence. At this stage, you should be working towards a 50/50 revenue split between recurring SaaS and transactional payments. As you continue to grow, buyers are likely going to put an even higher value on payments revenue. As Brad explains, “We try to make the argument that payments revenue can actually be more valuable than contracted SaaS—because it grows with customer activity.”

Characteristics of Top-Performing Embedded Payments Companies

Brad has seen a range of companies come through the pipeline over ten years at Software Equity Group and knows what good looks like.

“The perfect company is one that’s had payments revenue for three or four years, where you can see a steady cohort of growth and consistency, and improved retention over time.”

Here’s what the top-performing companies all bring to the table:

3–4+ years of payments history

Consistent cohort growth

High payment penetration

Strong retention metrics

Payments deeply embedded in workflows

A Strong Financial Profile:

Strong Rule of 40

High gross margins

Efficient growth (balanced burn)

If you meet these performance standards, you’ll earn strong interest from private equity groups. You’ll also be likely to have more competitive deal dynamics and reach your premium valuation potential.

“If you give me a pure SaaS company versus a SaaS plus payments company with those characteristics—I’m all over it. I know I can get the PE market really excited.”

Why Vertical SaaS Founders Should Act Now

Embedded fintech is becoming a standard, even an expectation, for vertical SaaS companies.

Keep in mind that mission-critical products will always command higher multiples. There is power in niche markets as well – as long as your product is a “must-have” not a “nice-to-have.” There’s a great opportunity in being number one in a small TAM. With niche dominance and payments, you’ll have strong defensibility.

Brad sees a number of high-value verticals on the horizon, including:

Real estate

Healthcare

Government

Manufacturing

EdTech

As the market continues to emphasize efficiency and monetization, keep these elements in mind as you build your embedded payments offerings and plan your exit strategy:

Traction beats vision when it comes to valuation

Deep integration beats surface-level add-ons

The best financial model combines SaaS stability and payments upside

By following this guidance, you’ll build a stronger business and create a more compelling exit story.

Payabli can be your partner to accelerate faster time to market, improve monetization and ensure a scalable embedded payments infrastructure. Schedule a demo with our payments experts today.

What a product marketer sees when a platform treats payments like a checkbox.

I market products for a living. When I joined Payabli as its first dedicated product marketer, my whole job became understanding who payments is for, what job it does for them, and how to say it so the right people actually care.

Which means I notice when something that should get that treatment doesn’t. In vertical SaaS, that something is almost always payments.

Most platforms don’t market payments. They just switch it on. It shows up as a toggle in account settings, a line on the pricing page, a “yes, we do that” in an RFP – and then everyone moves on. The work that any other product would get – figuring out who it’s for, what it does for them, how to launch it, how to prove it – never happens.

Here’s the distinction I keep coming back to. A feature is something you switch on. A product is something you do the work to understand, position, launch, and prove. And the product go-to-market work is the part I see most vertical SaaS platforms skip, because payments technically function the moment it’s enabled. It processes. A transaction goes through. It looks done. So nobody does the marketing – and then everyone wonders why merchants aren’t adopting.

Let me walk through the work that gets skipped. It’s all product marketing, and none of it is glamorous.

“Merchants” is not an audience

Once payments go live, most vertical SaaS platforms promote payments as a feature with a general announcement: “Payments are now available!” – sent to their entire merchant portfolio, identical copy, one and done.

But your merchants aren’t one audience. A solo practitioner who runs their whole business from their phone has nothing in common with a multi-location operator with a back-office team, except that they both pay you. They have different fears about payments, different reasons to adopt, different things that make them hesitate. A product marketer’s first move is to segment – to figure out which merchants have the most to gain and what specifically would move them – and then convey the different value propositions to each.

One generic blast isn’t a launch. It’s a notification. And notifications don’t change behavior.

Nobody wakes up wanting payments

This is the one I’d tattoo on every platform team if I could.

Merchants do not want payments. They want to get paid without chasing an invoice for three weeks. They want to stop reconciling two systems by hand every week. They want to stop losing a sale because the only option was “mail us a check.” Those are the things they want. Payments is just the mechanism.

Feature-thinking markets the mechanism: “We support ACH, cards, and digital wallets.” So what? Good product marketing markets the job that gets done: “Get paid the day you finish the work, not the month after.” Same capability – but one is a spec sheet and the other is a reason to care. The discipline here is brutally simple and almost nobody does it: take every payments feature you’ve got and run it through the “so what?” test until you reach something a merchant would actually feel.

Switching it on isn’t a launch

In a feature mindset, the moment the code ships, the job is done. In a product mindset, that moment is the starting line.

Adoption is its own motion, and a lot of it is product marketing: the in-product nudge at the moment a merchant would feel the pain, the activation sequence that walks them from “enabled” to “first transaction,” the milestone messaging when they hit their tenth payout. A product gets an adoption plan. A feature gets a changelog entry and a shrug.

And here’s the part feature-thinkers never get to: once you’re marketing adoption, you can actually measure which message works. Which value prop drives activation? Which segment converts? That’s message-market fit, and you only get to learn it if you treat the launch as something to market in the first place.

Your own team is your first market

Before a single merchant hears about payments, your own people have to be able to talk about it. Your CSMs, your support team, your account managers – if they can’t explain in one sentence why a merchant should turn payments on, no merchant ever will.

Payments adoption dies internally first. This is why internal enablement is product marketing, not an afterthought to it. Someone has to arm the people closest to the merchant. Otherwise the best positioning in the world never leaves the building.

Claims don’t travel without proof

The last thing a feature never gets, and a product always needs: proof. A platform will say “merchants love our payments” with nothing behind it. A product marketer’s instinct is to ask how do we know, and can we show it. Proof is what makes a claim portable. Without it, your messaging is just an assertion competing with everyone else’s assertions.

For what it’s worth, the proof we lean on at Payabli is scale: hundreds of billions of dollars moving across more than 100 vertical platforms. But the number only matters because we can point to what it did for the platforms behind it. A statistic with no story is just a feature in disguise.

The takeaway

Treating payments as a product isn’t about charging more for it. It’s about doing the work – knowing who it’s for, naming the job it does, marketing the launch instead of just shipping it, beating the status quo, arming your own team, and bringing proof.

That work is product marketing. It’s unglamorous, it’s mostly invisible when it’s done well, and it is the entire difference between payments that sit in a settings menu and payments your merchants actually adopt.

If you’re reading this thinking “we switched payments on a year ago and never really marketed it” – that’s not a problem, that’s the opportunity. Let’s have a conversation.

If you’re building embedded payables into your SaaS platform, you’ve likely hit the same bottleneck: getting vendors paid once a bill is approved.

Your merchants approve a bill and are ready to disburse, but the vendor hasn’t shared how they want to be paid. So the AP team starts calling and emailing to collect bank details and routing numbers, and an automated payout becomes days or weeks of back-and-forth.

This is where embedded payables stalls for most vertical SaaS platforms. The bill is approved and the funds are available, but the payment waits because collecting the vendor’s payment details is still a manual process. Your merchants fall back on chasing and check-cutting, your payables volume stays flat, and the revenue embedded in every transaction goes unrealized.

Vendor Payment Links remove the manual chase, making them the easiest way to get any vendor paid.

The manual chase that stalls every payout

Embedded payables only work when the payment can move, and that depends on collecting payment details from every vendor, one at a time.

For high-volume, repeat vendors, this is manageable. Many are glad to set up their payment preferences once and keep them on file, and a Vendor Portal is a strong fit for those ongoing relationships.

But much of your merchants’ vendor base doesn’t work that way. They’re one-time or infrequent payees serving dozens of customers across different platforms. Asking them to create a portal account for a single payment is friction they won’t accept, and the alternative – having AP teams collect details by phone and email – is slow, error-prone, and difficult to scale.

When that chase drags on, the effects compound:

For your merchants: Bills sit in “pending” while AP teams trade calls and emails to track down bank details. When a vendor is slow to respond, teams cut a manual check to close it out, and the automation your platform promised becomes a partial solution.

For your platform: Every payment stuck in manual limbo is a payment that doesn’t move through your rails – less transaction volume, less payment revenue, and a weaker position heading into renewal conversations.

For the vendor: They’re caught in the back-and-forth too, and often wait on a mailed check anyway. The slowest, least reliable method wins by default, simply because collecting their details took too long.

The answer isn’t forcing every vendor down the same path. High-touch vendors are well served by a portal, while one-time and infrequent payees need a faster, self-service way to get paid. Supporting both ensures every vendor is enrolled, regardless of how engaged they are.

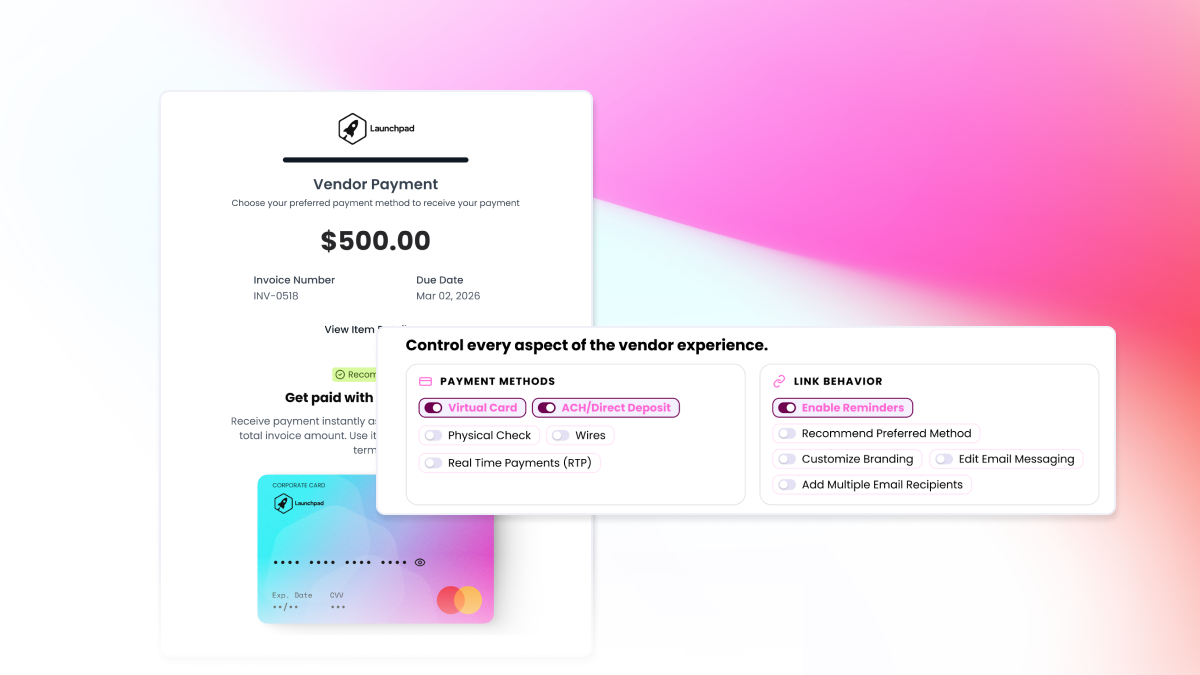

How Vendor Payment Links work

Vendor Payment Links flip the model. Instead of your merchants chasing vendors for details, each vendor receives a single, secure link that handles data collection and disbursement in one interaction.

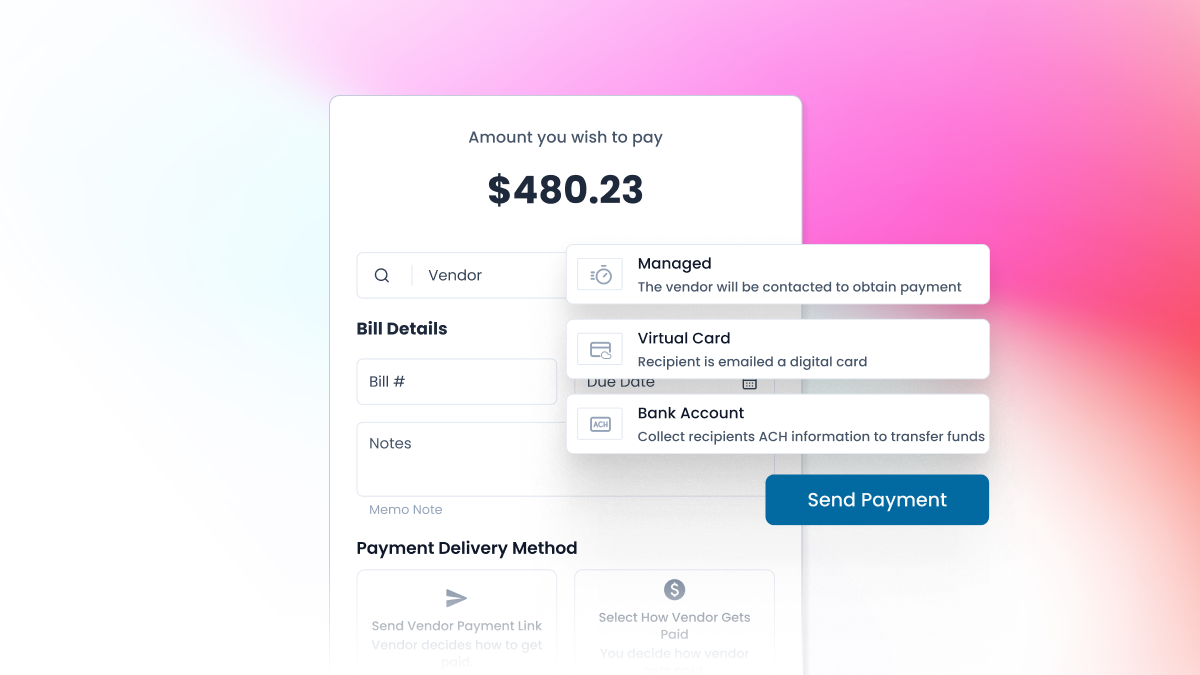

Step 1: A merchant approves a bill inside your platform, triggering a payment link to the vendor.

Step 2: The vendor receives a branded email with a secure payment link. Branding is configurable at the merchant or platform level; Payabli remains invisible.

Step 3: The vendor opens the link and selects a preferred payment method on a clean, hosted page – no account to create and no back-and-forth.

Step 4: Funds are disbursed automatically. The vendor’s payment preference is tokenized and stored, so future payouts happen without another link.

That final step is where the value compounds. Every link interaction builds a tokenized payment profile for the vendor: the first payment requires the link, and every payment after that is fully automated using stored credentials.

What can be configured

Vendor Payment Links give platforms and merchants granular control over the vendor experience, including which payment rails are offered and how each link behaves.

Payment methods are configurable per vendor or per link. Platforms can offer any combination of virtual cards, ACH/direct deposit, physical checks, wire transfers, and real-time payments (RTP), and can set a recommended default – useful for steering vendors toward virtual cards, where high interchange revenue flows back to your platform.

Link behavior is equally flexible. Merchants can enable automatic reminders for incomplete links, customize the branded email, add multiple recipients per vendor, and tailor the payment page to match their business’s look and feel.

Why this matters for platform economics

Every payment stuck in a manual chase is a payment that doesn’t move through your rails, and every payment that doesn’t move through your rails is revenue your platform is missing out on.

Vendor Payment Links remove the bottleneck entirely. When enrollment is self-service, more payments move through your rails, and more volume becomes revenue – through interchange sharing on virtual cards, markup on ACH, RTP, wire, and check fees, or simply stronger merchant retention because your payables product works end to end.

The option to recommend a preferred method also gives platforms a subtle but powerful lever. Defaulting to virtual cards, for example, steers volume toward the rail with the strongest revenue share without forcing the vendor’s hand. They still choose; you simply make the highest-value option the easiest to select.

The operational impact

Beyond revenue, Vendor Payment Links remove the operational drag of manually collecting and managing vendor payment details.

Fewer manual touchpoints. Rather than reaching out to each vendor and waiting for a reply, AP teams let vendors self-select their payment method through a secure link. Outreach happens once, automatically.

Higher data quality. When vendors enter their own verified details, merchants no longer key in bank information by hand, which means fewer failed payouts.

Healthier vendor relationships. Vendors who get paid quickly keep delivering without disruption. The link experience removes payment friction, so a slow payout never strains the relationship or stalls the service your merchants are counting on.

Vendor enablement that scales. Traditional enablement requires teams to call each vendor individually. That works for smaller portfolios but breaks down across hundreds or thousands of payments. Vendor Payment Links let vendors enroll themselves, with no outreach required.

Stored credentials remove repeat friction. After the first interaction, the vendor’s payment method is securely tokenized on their record, and future payouts reference it automatically. Platforms and merchants can set a default method per vendor so payouts flow without manual intervention.

Where Vendor Payment Links fit in the payables stack

Vendor Payment Links aren’t a standalone product – they’re the self-service collection layer that optimizes the rest of your embedded payables strategy. They give merchants and vendors a frictionless way to exchange payment details without phone calls, manual data entry, or a custom UI, so your platform can scale payouts without scaling manual effort.

Combined with Payabli’s broader Pay Out capabilities – bill management, approval workflows, AI-powered vendor enrichment, ghost cards for recurring vendor spend, and configurable funding models – Vendor Payment Links close the last-mile gap between “bill approved” and “vendor paid.”

Ready to eliminate the vendor payment chase? See how Vendor Payment Links fit into your embedded payables strategy at payabli.com/demo.

When it comes to embedded payments, one size never fits all. Every vertical SaaS platform has different technical capabilities, operational resources, growth timelines, and revenue goals. That’s why Payabli built our partnership approach around a single commitment: meeting you exactly where you are and growing with you from there.

Whether you’re launching your first payment feature or operating a full-stack payments business, Payabli gives you three paths to embedded payments – and the freedom to mix and match across all of them.

Embedded Payments Infrastructure Built for Where You Are – and Where You’re Going

Payabli’s embedded payments infrastructure is designed around how vertical SaaS platforms actually grow – not how a rigid vendor wants you to buy. You choose how you start, how deep you go, and how fast you move. And no matter which path you’re on, Payabli’s white-label solutions keep your brand front and center, so payments always feel native to your product.

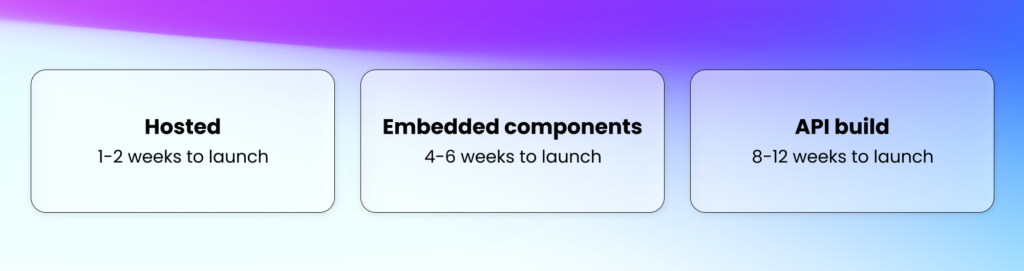

1. Hosted Solution: Launch in 1-2 Weeks with Minimal Lift

The goal: Go live fast with zero dev work and immediate revenue.

This is the fastest path to embedded payments – little to no engineering sprint required. With Payabli’s hosted solution, your customers click “pay,” land on a hosted payment page, and return to your platform. Simple, proven, live this month.

With Payabli, you can go live using:

Pre-built, hosted payment and onboarding forms that require minimal developer effort

White-label experience that keeps your brand front and center

Payabli-managed operations, including underwriting, onboarding, risk, and support – including end-to-end merchant support, so your team stays focused on your core product, not payment tickets

Start making money on payments immediately

You don’t need a payments team or a deep technical build. Plug in, go live, and start generating revenue while validating product-market fit.

Built for: Early-stage SaaS platforms, lean engineering teams, or any platform that wants to prove the payments opportunity before committing to deeper integration.

2. Embedded Components: Go Deeper & Gain Independence in 4-6 Weeks

The goal: Payments that live inside your platform – faster than a full custom build. Begin to take on more operational ownership at your own pace.

Once you’ve validated demand and built confidence in operating payments, embeddable components enable you to embed Payabli’s capabilities more deeply into your platform – making payments feel truly native to your product.

What this enables:

Payment widget, reporting, and boarding – easily enabled via no-code or low-code embedded components

Looks and behaves like you built it from scratch

Mix managed and self-service operations, handling some functions yourself while Payabli supports others

Tailor workflows around your industry’s specific needs

Enable more advanced features like custom pricing models, enhanced reporting, or additional payment methods

You get the native feel of a custom build at a fraction of the time and effort – a sweet spot between speed and sophistication.

Built for: Scaling SaaS platforms ready to differentiate their payments experience and develop operational muscle.

3. API Build: Full Control in 8-12 Weeks

The goal: Build the exact payment experience you want, with complete control over every detail.

For platforms ready to operate like a sophisticated payments business, Payabli’s API-first infrastructure gives you everything you need to run a full-stack payments operation. Every touchpoint, exactly as you designed it.

Operate your own risk program with granular controls

Build fully custom onboarding and servicing workflows

Own pricing, economics, and merchant lifecycle management

Automate end-to-end operations with deep technical integrations

Deliver a fully white-labeled payments experience from start to finish

You’re not just offering payments – you’re running a PayFac-level operation that drives significant value for your platform and your customers.

Built for: Mature SaaS platforms with dedicated payments teams treating payments as a strategic revenue driver.

The Real Differentiator: Mix, Match, and Scale

What makes Payabli unique isn’t any prescribed sequence – it’s that you can move fluidly between them, mix capabilities across them, and shift your approach as your business evolves. No rigid tiers. No outgrowing your provider.

With Payabli, you can:

Move at whatever pace makes sense for your platform

Mix and match capabilities – start with hosted, layer in embedded components, graduate to API when you’re ready

Shift operational responsibilities to your team or back to Payabli as your needs change

Choose your customer support model – let Payabli handle merchant support communications end-to-end while you own the merchant communication directly, or operate like a PayFac with Payabli behind the scenes while you own the merchant relationship directly

Scale without ever needing to re-platform

As Aaron Vela, Payabli’s Account Executive, puts it: “We align with you on service, operations, and technology all along the way. Whether you want to start small and scale gradually, or move quickly with advanced capabilities, our platform and team are designed to meet you exactly where you are.”

That flexibility isn’t a feature – it’s the foundation.

Why This Matters for Vertical SaaS: The Payments Platform You’ll Never Outgrow

Most payment infrastructure providers force a choice: oversimplified tools that cap your potential, or complex enterprise platforms that demand massive upfront resources. With With Payabli, you don’t have to choose – and more importantly, you never have to choose again.

There’s no ceiling on what you can build. No exit ramp that forces a costly re-platform when you scale. No tier upgrade that holds your next feature hostage. You launch at whatever stage makes sense for your business today, and the infrastructure grows with you.

You can:

Launch quickly without sacrificing future sophistication

Prove the payments opportunity before committing significant resources

Scale your investment in payments alongside your platform’s growth

Maintain full optionality to shift your approach as your business evolves

Never outgrow your provider – Payabli grows with you from day one

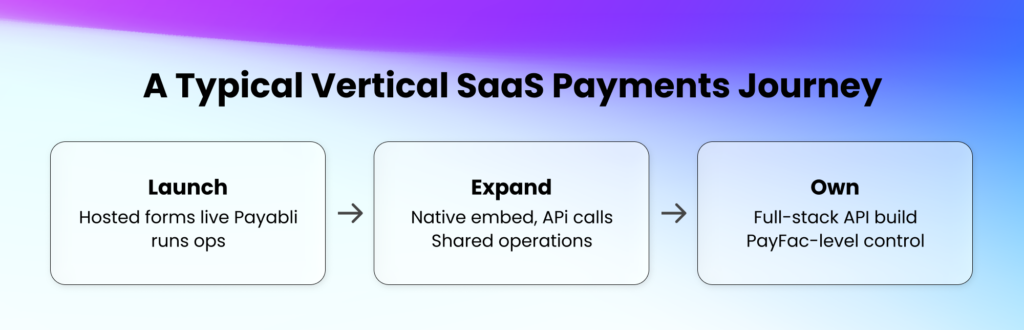

What the Vertical SaaS Journey Often Looks Like

Every SaaS platform is different, but here’s a common progression to revenue generation:

Months 1–6: Go live with hosted onboarding and payment forms. Payabli manages underwriting, support, and risk. You prove that customers want embedded payments and early revenue starts flowing.

Months 6–12: Integrate via API for deeper customization. Embed more workflows natively. Take on select operational tasks. Adopt new tender types, pricing models, or reporting tools.

Months 12+: Own risk, underwriting, and pricing end-to-end. Build tailored experiences for different merchant segments. Scale with fully automated workflows. Operate a full-stack payments business powered by Payabli’s APIs.

The pace and path are always yours to define. When the infrastructure doesn’t hold you back, there’s no limit to how fast you can grow:

“With Payabli’s simple APIs and Pay Out capabilities, we launched a payment solution for our end clients in record time, enabling us to facilitate millions of dollars in payments each month. Bringing an Accounts Payable product online has transformed our business — expanding into new markets, evolving into a fintech leader, and achieving more payment volume this year than all of last year combined.” – Aditya Kaddu, CEO and Founder at EdStruments

Ready to Start?

You don’t need a fully formed payments strategy to begin working with Payabli. You just need to take the first step. Whether you want to launch fast, go deep, or take full control (or start somewhere in between) – Payabli has the infrastructure, partnership, and flexibility to meet you there.

Schedule a demo and let’s talk about where you are today, and where you want to go on your embedded payments journey.

Guest Post by Ershad Jamil | Former CGO, ServiceTitan

Key takeaways

As AI makes software features easy to copy, embedded finance is the most durable layer vertical SaaS can own, because it ties your revenue to your customers’ transactions, not to whether they renew.

Embedded payments grow your revenue as your customers grow and make your platform far harder to leave.

The strongest platforms own three layers: a system of record, embedded finance (payment acceptance, accounts payable, and payment operations), and AI-driven workflows.

For the better part of the last decade, vertical software companies operated on a relatively simple and highly effective model: build a great product, charge a monthly subscription, and scale recurring revenue. It was clean, predictable, and, for many, incredibly successful.

But that model is starting to show cracks, and AI is accelerating the shift.

Why is subscription-only SaaS losing its edge in the age of AI?

We’re entering a world where software features are easier to build, faster to replicate, and increasingly commoditized. What once required years of engineering investment can now be developed in a fraction of the time. As that happens, the durability of pure subscription revenue comes into question. If your differentiation is primarily feature-based, it’s becoming harder to defend over time.

The pressure is not theoretical. AI use inside organizations climbed from 78% to 88% in a single year, and as those capabilities spread, the features that once set a platform apart get matched far sooner.

That doesn’t mean SaaS is going away. It means it’s no longer enough on its own.

How did embedded finance go from optional to essential?

Long before the current wave of AI, there was an emerging idea that many software companies initially resisted: embedding financial technology directly into their platforms.

A decade ago, this felt like a departure from the core SaaS playbook. Payments, in particular, introduced a very different monetization model. Instead of charging a fixed monthly fee, revenue became tied to customer outcomes. You made money when your customers processed transactions, when they got paid.

For founders used to predictable subscription revenue, that felt uncertain. It introduced complexity around compliance, underwriting, and operations. It wasn’t obvious that the tradeoff was worth it.

But over time, something important became clear. Software that helps businesses operate is valuable. Software that helps businesses make money and manage money is indispensable.

What turns a software feature into financial infrastructure?

Today, embedded FinTech is no longer a “nice to have.” It has become one of the most powerful levers for growth and retention in vertical software. When you enable a customer to accept payments, pay vendors, manage cash flow, and reconcile transactions directly within your platform, you move from being a tool to becoming part of their financial infrastructure. That shift changes everything.

Revenue becomes more aligned with your customer’s success. As they grow, you grow. As they process more transactions, your monetization expands naturally. Just as importantly, your product becomes significantly harder to replace. Financial workflows are deeply embedded, and once they’re integrated into daily operations, switching costs increase dramatically. This is why so many of the most successful vertical SaaS companies today are also, in many ways, financial platforms.

Does AI replace embedded finance, or amplify it?

There’s a tendency to think of AI as a replacement for traditional software value. In reality, it’s more of an accelerant. AI is transforming how work gets done inside software. It can automate scheduling, follow up with leads, generate invoices, and even assist in closing sales. But all of those workflows ultimately lead to a single outcome: a transaction. And transactions require infrastructure.

As AI increases the speed and volume of business activity, the importance of seamlessly handling payments, payouts, and financial operations only grows. You don’t just need to enable transactions. You need to manage them intelligently, reconcile them in real time, and provide visibility into what’s happening across the business.

What does the modern multi-product SaaS platform look like?

What’s emerging is a new standard for vertical software companies. The most resilient platforms are no longer built around a single product or revenue stream. They combine multiple layers of value:

This combination creates a powerful dynamic. AI increases efficiency and drives more activity within the platform. Financial infrastructure monetizes that activity. And the core software anchors everything in a single, cohesive experience. The result is a more diversified business model, stronger customer alignment, and a much more defensible position in the market.

Why is payment infrastructure the unlock?

Despite the clear benefits, building financial technology in-house is not trivial. It requires navigating regulatory requirements, managing risk, supporting multiple payment methods, and building the operational backbone to handle it all. That’s where infrastructure providers have become critical to the ecosystem.

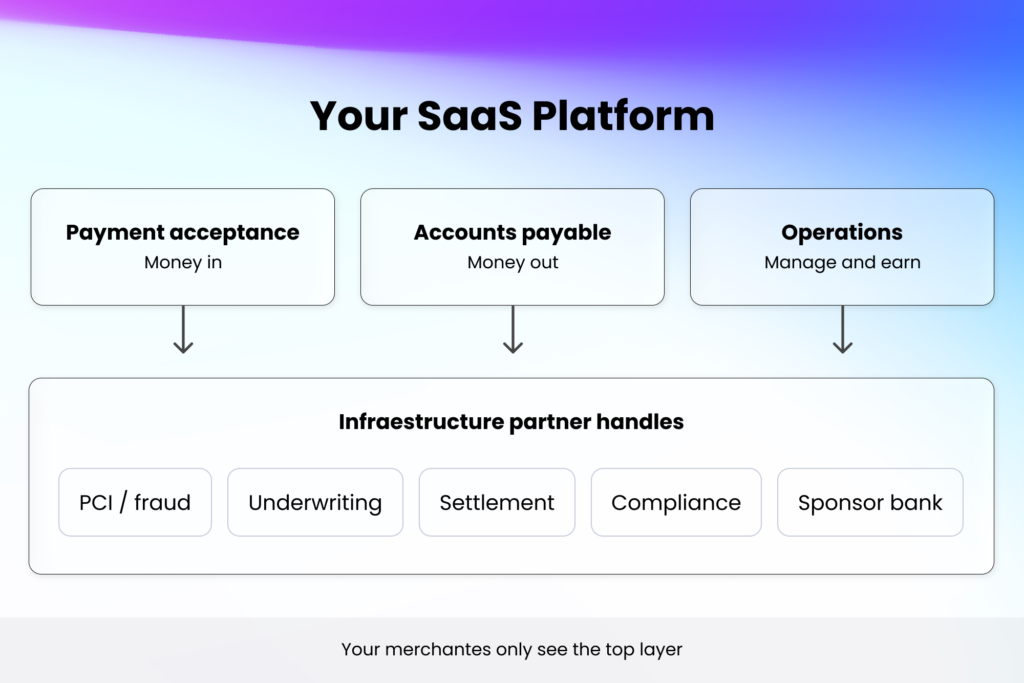

Companies like Payabli are designed to abstract away that complexity. By offering capabilities like Pay In, Pay Out, and Pay Ops in a unified platform, they allow software companies to embed financial functionality without having to become full-fledged payments companies themselves.

This isn’t just about faster time to market, though that matters. It’s about enabling software companies to deliver a seamless, end-to-end experience for their customers, from the moment work is created to the moment money moves and is reconciled. And the opportunity sits squarely with this layer: Bain estimates revenue for software platforms and the infrastructure powering embedded finance has roughly doubled, from about $22 billion in 2021 toward $51 billion.

What does it mean to become an economic platform?

The broader shift happening right now is not just technological, it’s structural. Vertical SaaS companies are evolving from software vendors into economic platforms. They’re not just enabling workflows; they’re participating directly in the financial lifecycle of their customers’ businesses. That shift fundamentally changes how value is created and captured.

In a world where AI continues to compress the advantage of pure software features, the companies that win will be the ones that go deeper, those that own not just the workflow, but the outcomes tied to it.

AI will reshape software in profound ways. It will make products smarter, faster, and more capable than ever before. But it won’t change the fundamental reality of how businesses operate. Companies still need to get paid. They still need to move money. They still need clarity and control over their financial operations. The opportunity, and increasingly the requirement, is to bring all of that into a single, cohesive platform.

Because in the next era of software, it won’t be enough to simply power the workflow. You have to power the business behind it.

How does Payabli complete the stack?

Payabli provides that layer for vertical software companies. A single API unifies payment acceptance, accounts payable, and payment operations, so a platform can embed and monetize payments without the cost or complexity of becoming a full payments company. Platforms that have made the move see it in their numbers, from Builder Prime’s 1,000% increase in payment volume toSunbound moving payor adoption from 50% to 90% in under a month.

If embedded finance is the layer you’re ready to own, book a demo to see what it looks like for your vertical.

And stay tuned for my next article in the series: why the cost-reduction story is only half of it, and how AI is becoming one of the most powerful revenue levers a platform can pull.

Embedded payables let vertical SaaS platforms run automated vendor payouts inside their product, turning every outbound payment into a revenue stream for the platform and a faster, fully branded payout for the software customer.

B2B ACH (electronic bank-to-bank payments) volume grew nearly 10% in 2025, with close to 8.1 billion B2B payments as businesses continue moving away from paper checks. That volume is the wave that embedded payables ride.

A single API that covers payment acceptance, accounts payable, and payment operations keeps margin, data, and reconciliation under one roof, so adding accounts payable later does not mean onboarding a second vendor or rebuilding your reporting layer.

Owning the outbound side gives the platform a complete view of money flowing through the software customer’s business — in and out — in one place.

Embedded payables let vertical SaaS platforms earn on the money their software customers send out, not just the money they collect. Vendor and subcontractor payouts still run through bank portals, AP tools, and paper checks that the platform never sees. This guide covers how the model works, what platforms earn on each rail, and what to evaluate in a partner.

What are embedded payables for a SaaS platform?

Embedded payables are vendor disbursements that run inside your SaaS product instead of outside it. The software customer approves a bill, the system pays the vendor through the rail the vendor prefers, and the platform earns on the transaction. The per-transaction margin, the vendor data, and the workflow all stay with the platform instead of routing to a third-party tool.

This is the half of embedded B2B payments that most vertical SaaS platforms have not yet captured. Acceptance (Pay In) was the obvious first move because software customers were already collecting money. Payouts are where the software customer’s weekly workflow actually lives, which is exactly why owning them changes the platform’s relationship with its customer.

Where embedded payables show up in a vertical SaaS workflow

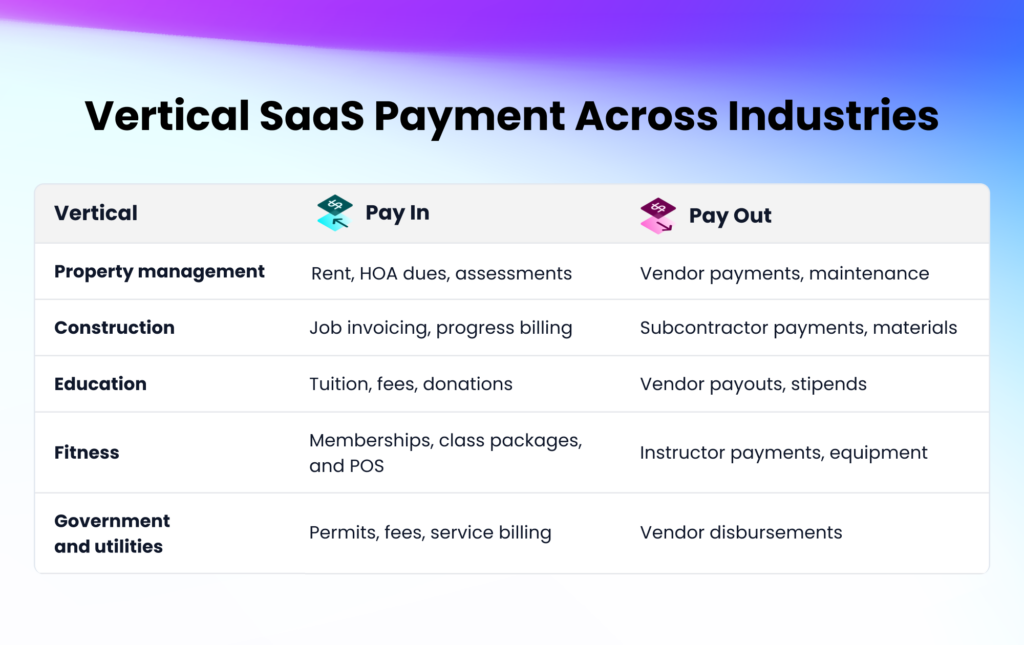

The pattern is the same across need-to-pay verticals, just with different vendors at the end of the line. A property management platform pays HOA service vendors and association contractors. A construction platform pays subcontractors and material suppliers on weekly draw schedules. A utility billing or field service platform pays the technicians and crews completing the work order. In every case, the payout sits one click away from the workflow the software customer is already using, and the mechanics behind that one click are what turn it into platform revenue.

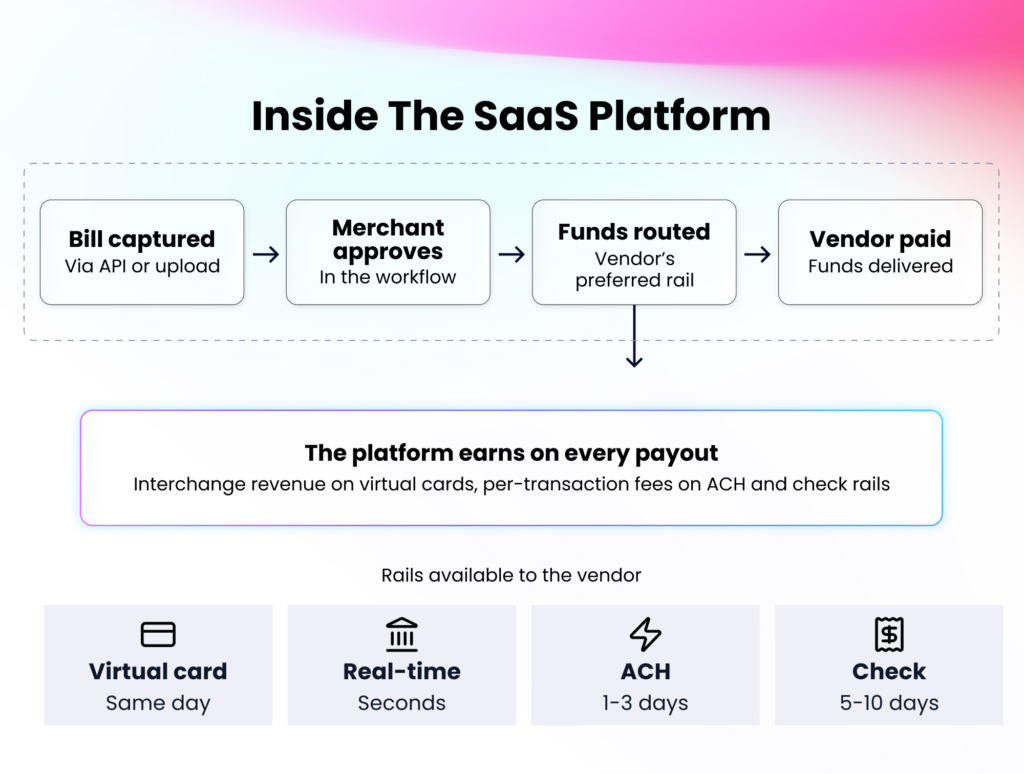

How do automated vendor payouts work for SaaS?

A bill enters the system, the software customer approves it, the payment routes through the vendor’s preferred method, and the data posts back to your platform with full remittance details. One API handles the money movement, webhooks fire at each status change, and the activity flows into the same reporting as your acceptance side.

How does money move from your platform to a vendor or subcontractor?

Funds debited from the software customer’s bank account move through whichever rail the vendor accepts (virtual card, ACH, check, RTP, and wire transfers), and settle to the vendor through the partner’s custodial account. ACH (Automated Clearing House) is the bank-to-bank network most vendor payments still ride on. The software customer sees the same status the platform sees, in near real time, without leaving your product.

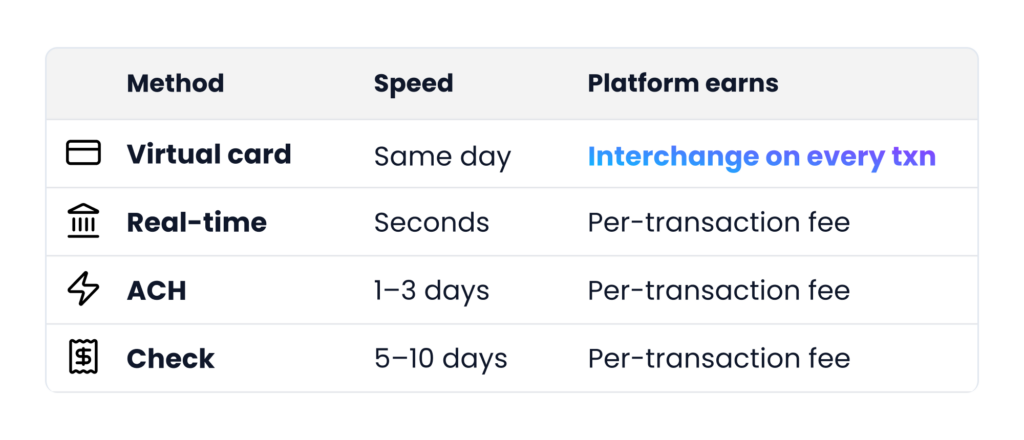

What payment methods can vendors actually receive?

Vendors can be paid through five rails, each with a different speed and platform revenue:

The shift toward digital rails is well underway. According to Nacha, B2B check usage fell from 81% in 2004 to 26% in 2024.

Virtual cards are digital card numbers issued for a single payment or vendor, and every transaction earns the platform interchange, a small percentage of the payment amount. For recurring vendors, Ghost Cards extend that earning model across the full year.

Who handles vendor enrollment and onboarding?

The embedded payments infrastructure partner runs vendor enablement through the product. Onboarding new payees is a configured workflow inside your software, not a manual process for your software customers or a support ticket for your team. Software customers focus on approving payments, not chasing banking details.

For situations where self-service makes more sense, Vendor Payment Links remove the enrollment step entirely. Your software customers send a secure link, the vendor enters their payment details, and funds are disbursed automatically. Collection and disbursement happen in one flow, with no portal to maintain and no enrollment to chase.

What are the benefits of embedded payables for SaaS platforms?

Four benefits drive the case for embedded payables: outbound revenue, stronger software customer retention, transaction data the platform owns, and a vendor experience under your brand.

1. Direct revenue on outbound volume

Every vendor payment earns the platform something. Virtual cards return interchange. ACH, checks, and instant payments return per-transaction fees. For most B2B software customers, outbound volume rivals inbound, which doubles the addressable revenue per customer.

2. Higher net revenue retention (NRR)

Approving bills, managing vendors, and reconciling payments are weekly tasks. When they run inside the software, the platform stops being a tool and becomes a workflow, which is what protects NRR.

3. Transaction data the platform owns

Every payout records which vendor was paid, when, on what terms, and through which rail. That dataset is what unlocks future products like cash flow forecasting, vendor scoring, and working capital.

4. A branded vendor touchpoint

Vendors get paid through the rail they prefer and see the platform’s brand on the remittance. The software customer looks more professional to their own vendors, and the platform’s brand reaches beyond its direct customer base.

What should you look for in an embedded payables solution?

The right embedded payables partner protects your margin, your brand, and your software customer relationship. Three questions cut to whether one fits.

Does it handle vendor enrollment without adding work to your team?

A strong partner runs vendor enablement inside the product, so onboarding new payees is a configured workflow rather than a manual lift for your software customers or a ticket queue for your support team. Enrollment is also where virtual card adoption is won or lost, because every vendor who never gets enrolled is a vendor who keeps getting paid by check, which is the lowest-margin rail on the stack.

Does it support the rails your vendors actually want?

Virtual cards earn the most, but vendors will still ask for ACH and checks. A solution that supports all three lets your platform earn across the full rail mix instead of forcing every vendor onto one method. Real-time payments and wire transfers are the next rail to evaluate, because instant settlement is becoming table stakes in verticals like construction and field service, and the platforms that support it earn on a transaction tier their competitors cannot match.

Does it cover payment acceptance and accounts payable on one stack?

If acceptance is already live, the accounts payable layer should plug into the same API, the same reporting, and the same reconciliation. Splitting them across two vendors fragments software customer pricing, doubles the engineering surface your team has to maintain, and leaves no single partner accountable when margin or reconciliation issues come up. The unified stack is also what makes future products like cash flow forecasting and working capital monetization possible, because both sides of the software customer’s money flow are sitting in one dataset under your control.

How to add embedded payables to your SaaS platform

The integration choice shapes how fast you ship and how much engineering you spend doing it. The right path depends on engineering bandwidth, brand control needs, and how fast you want to start earning on outbound volume.

What integration options can you choose from?

Embedded payables ship through multiple integration paths, ranging from fully custom API builds to prebuilt, ready-to-launch options. Each varies in time to launch, level of UX control, and the engineering investment required. Your provider can walk you through the options that fit your team’s capacity and timeline.

Sunbound launched embedded payments with a single developer and one project manager in under two months and now processes over $1 billion in annual payment volume. For a deeper look at how to sequence the integration, see embedded payments best practices.

How do you pick the right path?

The answer is to pick the path that gets you to live software customers fastest, then upgrade later. Revenue on outbound volume only starts compounding once real payments are flowing, and waiting for a more complex build means months of forgone interchange. Most platforms that start lean ship significantly faster than the ones that try to build everything upfront.

What does your team focus on during rollout?

The provider handles compliance, sponsor banking, and risk monitoring. Your team focuses on the product decisions: who can approve payments, how funds are sourced, what the vendor experience should look like, and how reporting surfaces inside your existing dashboards. Most rollouts run on a weekly cadence with the partner during the build phase, then taper to monthly check-ins once the integration is live and software customers are flowing through.

How Payabli turns vendor payouts into a revenue stream for SaaS

Payabli offers payment infrastructure and monetization for vertical SaaS platforms. Our Pay In / Pay Out / Pay Ops framework unifies payment acceptance, accounts payable, and payment operations under a single API, so platforms capture both sides of their software customers’ money flow without managing multiple vendors or rebuilding their reporting layer.

Virtual cards, ACH, checks, real-time payments, and wire transfers are embedded alongside acceptance flows on the same integration. Vendor enablement, invoice intake, and configurable approval workflows are built in, so software customers see a polished, fully branded product from day one.

Vertical SaaS platforms in property management, construction, utilities, education, and government use Payabli to turn vendor payouts into platform revenue.

If you are mapping where embedded payables fit on your roadmap, book a demo to see what your platform’s payout volume could earn.

I’ll be upfront. I didn’t come up through the payments industry. My background is operations and strategic leadership – the discipline of taking something that works inconsistently and making it work every time, at scale.

When I joined Payabli nearly four years ago, the company was a small group of scrappy entrepreneurs and a few early adopter partners that believed in the future of embedded payments. Today we’re moving hundreds of billions of dollars across over 100 vertical software platforms serving industries from property management to field services to legal.

I’ve had a front-row seat to what separates embedded payments programs that scale from ones that stall. It almost always comes down to four things:

How you implement

How you onboard

How you scale

What you do after go-live

Here’s what I’ve learned about each.

Integration: Implementing for the Long Haul

The first place a payments partnership is won or lost isn’t at the signing table. It’s in the integration.

Every week a partner spends in an integration cycle is a week their merchants are still on a legacy processor, not processing on your platform, and not generating revenue for anyone. Delayed launches don’t just push timelines. They erode confidence. Merchants who expected to go live in October and are still waiting in December start questioning whether they made the right call. Some of them churn before they ever process a single transaction.

The root cause is almost never a bad API. It’s an incomplete product:

Documentation that doesn’t match live behavior

Sandbox environments that don’t reflect production edge cases

A support model that treats integration questions like tickets in a queue instead of blockers with real business impact

At Payabli, our solutions engineering function exists to close that gap before it opens. We scope integrations before a line of code is written, and we ask harder questions upfront:

What does your merchant population look like at scale?

What billing models do you need to support?

What does your support team need to handle merchant issues without escalating to us?

Those answers define the integration. Skip them, and you ship something that works in a sandbox and breaks in production. Speed without completeness isn’t a win –it’s a delayed problem. At Payabli, we don’t trade one for the other.

Merchant Onboarding: From Application to Activation

Once the integration is live, the clock starts again – this time on every merchant waiting to go live.

Merchant onboarding is not just a compliance function. It’s a revenue acceleration function. Every merchant sitting in a pending queue is lost volume. Every onboarding flow that requires manual and time-consuming steps to complete is a merchant who might not finish. Configuration matters here just as much as speed: the right MCC codes, the right processing limits, the right fee structure tied to the partner’s program – these aren’t back-office details, they’re the foundation of a strong merchant relationship.

Underwriting plays a central role that often gets undersold. The goal isn’t just to approve merchants – it’s to approve the right merchants quickly and catch the wrong ones cleanly. A well-structured underwriting policy can clear the majority of merchants automatically, based on defined risk thresholds and data signals, without human intervention. That’s not cutting corners. That’s building a system that scales without adding headcount every time a partner adds merchants.

The outcome of a well-run onboarding process is a merchant who is approved, configured, and activated – processing their first transaction within days of applying, not weeks. Activation rate is the metric we obsess over because it’s often the first signal of whether a payments program is actually working.

Scaling Merchant Migrations: The Bulk Boarding Advantage

Bulk boarding is what happens when a platform has a mature merchant base and needs to move fast. It’s not a variation of standard onboarding – it’s a different operational model entirely, and one of the most powerful capabilities in embedded payments when it runs right.

It’s built for platforms migrating off legacy processors, launching payments to an existing customer base, or absorbing merchants from an acquisition. The merchant list already exists. The business relationship is established. What’s needed is a fast, clean path from data submission to live processing – at volume.

The difference between bulk boarding done well and done poorly is almost entirely operational.

Done poorly: a partner submits a merchant file, gets a spreadsheet back days later with 40% flagged for manual review and no explanation, and starts fielding support calls they can’t answer.

Done well: a clean intake template, automated validation, an intelligent underwriting layer that approves the majority instantly, and real-time visibility into every merchant’s status.

For Payabli, bulk boarding is a genuine competitive differentiator. It’s what lets a partner with 2,000 merchants convert their entire base in weeks instead of quarters. Whether it’s 30 new customers or 30,000+ migrating at once – I’ve seen it, and we’ve executed.

Post-Live Enablement: The Metrics That Matter

Most implementation conversations end at go-live. Ours don’t.

Getting merchants live is the prerequisite. The actual value of an embedded payments program is built in the months after launch – and it’s measurable:

Activation rate tells you if merchants are crossing the threshold from approved to processing.

Ninety-day volume tells you if they’re ramping or stalling.

Feature adoption – ACH, recurring billing, payouts – tells you how deeply payments are embedded in the merchant’s workflow.

Merchants who use two or more payment rails have materially higher retention than those who only accept card. That’s not an accident – it’s a function of how integrated payments become in their day-to-day operations. Chargeback rate and dispute patterns are merchant experience signals, not just risk metrics. When dispute rates spike for a cohort, there’s usually friction in the payment flow that nobody’s reported yet. Finding that early keeps merchants on the platform – and keeps partners from getting uncomfortable calls.

At Payabli, we help our partners track all of this – not as a reporting exercise, but because these metrics are the early warning system for churn and the playbook for growth. Vertical SaaS platforms who know their activation rate, 90-day volume, and product adoption curve can have confident conversations with their own leadership. Platforms who don’t are flying blind.

The Takeaway

Implementation is the moment of truth in any payments partnership. The platforms that win in embedded payments are the ones that treat implementation as a competitive advantage, not a line item.

If you’re reading this and thinking “I wish our current payments provider talked like this” – let’s have a conversation. That’s exactly where we should start.

Financial infrastructure is how vertical SaaS platforms monetize the transaction volume already flowing through their product by owning payment acceptance, accounts payable, and the operations that connect them.

Most SaaS platforms only earn from the money their merchants collect. Financial infrastructure opens a second revenue channel for the money merchants send, through the same integration.

Fintech-led vertical SaaS companies hold the strongest retention profile of any category, with 96% gross retention versus roughly 90% for other product types.

The right financial infrastructure strategy starts with auditing, where money already moves through your product, not with picking a vendor.

Subscription revenue only grows when you add new customers. Financial infrastructure revenue grows every time your existing merchants process a transaction. Median SaaS growth rates have settled at 26%, down from 30% two years ago, and net revenue retention across the industry has compressed to 101%. The SaaS platforms pulling ahead are not adding features. They are building a financial layer that earns on every transaction their merchants process.

This blog covers what financial infrastructure means for a SaaS platform, how it generates revenue, and how to build a strategy around it.

What is financial infrastructure for a SaaS platform?

Financial infrastructure is what lets your SaaS platform accept, send, and earn from your merchants’ money. It covers three functions: payment acceptance (Pay In) from your merchants’ customers, accounts payable (Pay Out) to their vendors and partners, and the operational layer (Pay Ops) connecting both, including onboarding, underwriting, risk, billing, and reconciliation.

Financial infrastructure vs. payment processors

A payment processor handles one job: moving money from point A to point B. Your SaaS platform sends a transaction, the processor routes it, and a third party collects the margin.

With financial infrastructure, the economics start to shift. Your platform sets merchant pricing, the infrastructure partner processes through a unified API, and you keep the spread between the two. You also own the transaction data, which means you can optimize pricing by segment and track adoption across your merchant base.

What makes financial infrastructure a revenue layer for SaaS?

Subscription revenue grows when you add customers, while payment revenue through financial infrastructure grows when your existing customers grow, with no upsell and no new contract.

That compounding dynamic is why fintech-led vertical SaaS companies hold the strongest retention profile of any category, with 96% gross retention versus roughly 90% for other product types, according to the benchmark report by Tidemark. The more financial workflows a merchant runs through your SaaS platform, the better their experience, the more revenue you earn, and the harder your product is to replace.

How does financial infrastructure actually generate revenue?

SaaS platforms generate revenue from financial infrastructure on two sides: the money their merchants collect and the money their merchants send. Most platforms only monetize the first.

Transaction spread explained: where SaaS payment margin comes from

Every payment your merchants process through your SaaS platform has an underlying cost. Your platform charges your merchants a rate above that cost. The difference is your margin.

That margin exists on both sides. On the Pay In side, you collect margin on every transaction your merchants collect. On the Pay Out side, when merchants pay vendors through your platform, you earn on each outbound payment too.

In practice, the key variable in SaaS payment margin is not the rate. It is volume. A SaaS platform with 200 merchants processing $300,000 each annually sits on $60 million in volume. That is revenue your subscription model cannot produce without adding new customers.

Which vertical SaaS industries earn the most from embedded payments?

In vertical SaaS, the highest-value financial infrastructure opportunities sit in industries where merchants cannot operate without processing payments through the platform. Here are some of the verticals where SaaS platforms generate revenue on both sides:

How do you build a financial infrastructure strategy for SaaS?

Most SaaS platforms pick a vendor before they know what they are monetizing. The sequence below starts with scope, not technology.

Step 1: Audit where money already moves through your product

Before evaluating vendors, define the scope of your financial infrastructure. Map where merchants collect money, where they send it, and where they leave your product to do either. That map determines whether you start with acceptance only or launch with acceptance and accounts payable together.

Step 2: Choose your integration model

There are three primary paths. A hosted solution gets you live in one to two weeks with minimal engineering lift — Payabli manages underwriting, risk, and support while you start generating revenue immediately. Embedded components go deeper, embedding payments natively into your platform in four to six weeks, with the flexibility to take on more operational ownership at your own pace. An API build gives you full control over every touchpoint — custom underwriting, risk, pricing, and merchant lifecycle management — for platforms ready to operate like a full-stack payments business.

What makes Payabli different is that you’re not locked into one path. You can start hosted, layer in embedded components, and graduate to API when you’re ready — without ever needing to re-platform.

Step 3: Set pricing and revenue share that scales with your merchants

Your pricing model shapes your margin at every scale. Payabli gives you full visibility into your cost structure so you can build pricing around your vertical, not a generic blended rate, and set different rates for different merchant segments. Whether you’re running flat rate, tiered pricing, or interchange plus, the right infrastructure gives you the pricing tools and cost transparency to make this practical from day one.

Step 4: Make payments the default

None of this matters if your merchants don’t actually activate. Payments should show up where the work happens, inside the invoice, inside the vendor payout, not behind a settings tab. Set enrollment as the default during onboarding and track merchant activation rate from day one. Activation rate is the percentage of your merchants actively processing through your platform. It belongs next to retention and NRR on your dashboard.

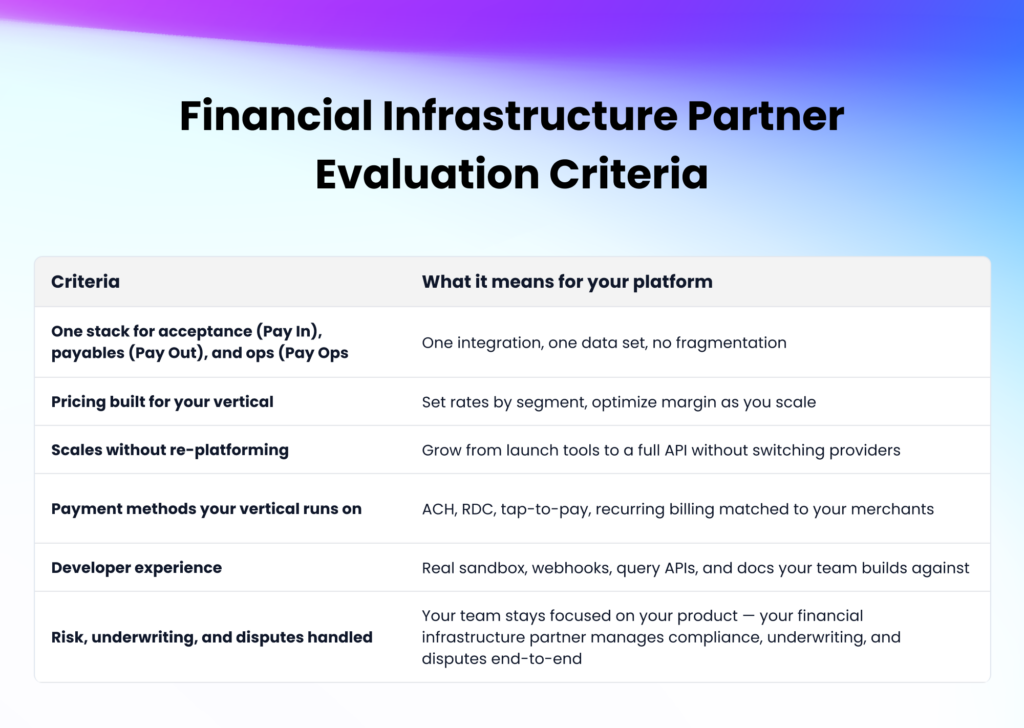

How do you evaluate a financial infrastructure partner for SaaS?

You have the strategy. Now you need a partner who can execute it. Get this wrong, and you rebuild.

How can Payabli help build your SaaS financial infrastructure?

Payabli was built to help vertical SaaS platforms do exactly what this blog describes. Payment acceptance, accounts payable, and payment operations run through a single API, so you do not stitch together three vendors to cover what should be one infrastructure layer.

Beyond the integration, Payabli gives you full visibility into your cost structure, segment-level pricing controls, and interchange optimization guidance so your platform is built to capture margin from day one. Every partner gets a dedicated payments team that knows their vertical and helps shape a go-to-market strategy around payments — not a generic onboarding checklist. The conversation starts with where you are and where you want to go, not with a product pitch.

Request a demo, and we will map the financial infrastructure opportunity for your platform.

Brad Weekes, Managing Director at Software Equity Group, brings a deeply informed perspective on how fintech is reshaping vertical SaaS business models and valuations.

Drawn to the intersection of technology, strategy, and finance, Brad has tracked the rise of integrated payments for over a decade. He spent his early years analyzing public markets while building a deep, hands-on understanding of software. He helped acquire companies, scale operations, and ultimately navigate the full lifecycle—from growth to acquisition and IPO.

Today at Software Equity Group, Brad advises B2B SaaS and embedded payments companies, typically in the $5M to $50M ARR range, on majority transactions and exit strategy.

The Shift from SaaS to Embedded Fintech

Back in 2018, Brad recalls working with a higher education software company. The company’s core offering allowed people to register for classes online. However, in the registration workflow, when payment was due for the class, the company handed the course registrant off to another provider to accept the payment. It was a classic scenario at the time, and one that sparked a conversation during the valuation process and with buyer conversations about how payments could be embedded in the workflow. The acquiring company spent a lot of time on payments, far more than there was any revenue to show for it.

Eight to ten years ago, vertical SaaS companies were starting to think about integrating payments as part of their offering and acquiring companies were intrigued. Today, payments are no longer optional. They are a primary driver of value.

Knowing embedded payments should be core to your product and its future is one thing, but actually executing on an embedded payments strategy (or additional fintech offerings) requires planning and execution.

From a product perspective, Brad notes it’s never too early to add payments. In fact, if you start too late, you won’t have the adoption rates or revenue proof points needed.

“You need traction—not a story.”

When it comes to customer adoption, that’s where timing really matters. Brad stresses that traction matters more than vision. He warns that buyers will discount “story-only” opportunities.

Beyond payments, fintech offerings like lending (marketplace-driven) and insurance (growing quickly) are emerging as additional value drivers. But, payments still remain the most proven and scalable entry point.

If you’re a vertical SaaS founder starting or evolving your payments and embedded fintech offerings, Brad suggests you keep a few payment-specific KPIs in mind.

Payments-Specific Metrics:

Payment penetration (critical)

Total payment volume (TPV)

Net take rate trends

Cohort adoption over time

Common Mistakes Founders Make

When embedding payments into your product to boost valuation and increase exit opportunities, there are a few simple mistakes you can easily avoid.

Brad has seen founders say, ‘‘we’ll just plug in payments here,” but he cautions it’s not that easy. There’s a lot underneath the hood. Here’s Brad’s quick guide to common payments mistakes and how to avoid them.

Underestimating Complexity

Risk: Payments ≠ simple plug-in

Opportunity: Think through operational, compliance, and go-to-market challenges

Low Penetration Across Customer Base

Risk: Starting too late to gain traction and build strong adoption rates. Reduces credibility. Opportunity: Embed payments early. Draft and execute an adoption playbook.

Treating Payments as a Bolt-On

Risk: Lack of deep workflow integration

Opportunity: Make payments a critical part of the workflow. The stickier payments are, the harder they are to rip and replace.

Why Embedded Payments Increase Company Value

Seeing how embedded payments drive immediate revenue, increase retention, and expand gross profit, it’s no surprise they are a primary driver of value. As Brad notes, embedding payments is effectively “found money” from your existing customer base.

“These SaaS companies find a new revenue stream with payments—often overnight. If they have an existing install base, they flip the switch on payments and NRR goes through the roof, and their gross profit grows dramatically.”

Embedded payments also help deepen product integration and customer retention. Your solution shifts from being a tool to a mission critical system thanks to tightly integrated workflows.

You also unlock new ways to monetize customer activity. The typical SaaS model is usage-based – depending on growth of seats. With embedded payments, you’re opening up possibilities of usage-based and outcome-based pricing.

“Now you have not only the software platform, but payments—which is a critical part of the workflow. Ripping that out becomes much more difficult.”

To ensure you maximize your valuation, Brad suggests you keep a few of these key metrics strategic buyers will scrutinize in mind.

Financial Metrics

Gross revenue vs. net revenue

Gross margin of payments stream

Cost structure (processing, interchange, etc.)

SaaS + Payments Combined Metrics

Net Revenue Retention (NRR)

Gross Revenue Retention (GRR)

Rule of 40

Gross margin profile

As you build out your embedded payments offering and your overarching pricing models, Brad does caution not to get too creative. He’s seen a few founders over-optimize pricing models (i.e. “free SaaS, monetize only payments’) to the point that it creates a lack of revenue stability and buyer skepticism.

“When you get too creative, you add noise. Buyers start asking, ‘why are you doing this?’ It just creates more questions than value.”

SaaS companies are facing a lot of pressure today as AI takes over that pricing models should be more outcome-based. There’s two sides to that coin because while buyers and investors might find the increased gross profit margin attractive, it’s likely that if you view that revenue stream like an annuity it’s not considered as valuable as contracted SaaS.

When we get a payments company with transaction or usage based activity, we try as much as we can to make it look like contracted recurring revenue. We want this payments revenue stream to look exactly like this recurring SaaS stream. Brad often argues embedded payments revenue is better because the NRR goes through the roof compared to contracted SaaS, which is limited by price increases that are CPI basis.

Tracking these metrics isn’t just good hygiene — it’s how you build a credible exit narrative. To make it easier, we put together a Payments Cohort Analysis Template you can use to track payment penetration rates, TPV trends, net take rate, and cohort adoption over time. It’s built around the exact data points acquirers will ask for.

Multiples can vary dramatically — working with an investment banker who understands embedded payments and can shape the narrative around your payments business may significantly improve your outcome

The best model combines:

SaaS stability

Payments upside

Deep integration beats surface-level add-ons

Start early — but execute thoughtfully

Ready to Build Payments Into Your Platform?

Brad’s advice is clear: the window to get ahead of this is now. Payments aren’t a feature you add when you’re ready to sell — they’re the infrastructure that makes your platform worth buying.

If you’re a vertical SaaS company looking to embed payments the right way — with the workflow integration, compliance backbone, and financial infrastructure that actually moves the needle on valuation — that’s exactly what Payabli is built for.

Without IVR payments, vertical SaaS platforms miss a major revenue channel. Payment-related calls can account for roughly half of inbound call volume in many businesses. Adding IVR captures those transactions, cuts merchant costs, and deepens platform stickiness.

IVR payments let customers pay by phone through an automated system using their keypad or voice prompts, with no live agent required and 24/7 availability.

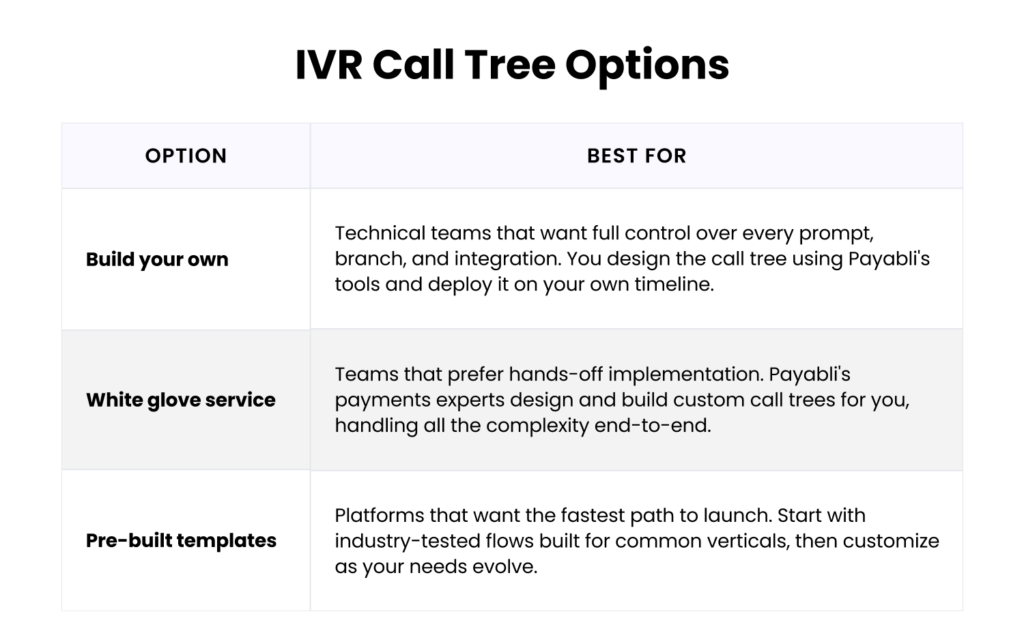

Call trees are the branching logic that shape each caller’s experience. With Payabli, platforms can build their own, use white-glove design services, or launch from pre-built industry templates.

Adding IVR alongside digital channels creates omnichannel payment coverage, which correlates with stronger merchant retention.

Most vertical SaaS platforms building embedded payments focus exclusively on digital channels like web, mobile, and payment links. But here’s what they’re missing: in many businesses, payment-related calls account for around 50% of inbound call center volume.

This represents a massive opportunity. Adding IVR payments lets you capture transaction volume competitors miss, reduce merchant operational costs, and create deeper platform integration that drives retention.

But what exactly are IVR payments? How do call trees guide the customer experience? And why do they create such powerful switching barriers for SaaS platforms chasing embedded payments revenue?

In this article, we explain what IVR payments are, how call trees guide the customer experience, and the strategic benefits for your platform.

What are IVR payments?

Interactive Voice Response (IVR) payments let customers make secure credit card and ACH payments over the phone using an automated system, with no live agent required. Customers call a secure phone number, follow voice prompts, or use their keypad to enter payment information, and receive instant confirmation.

Think of it as a virtual terminal that customers operate themselves through their phone, available 24/7/365. Because the caller enters card data directly via DTMF tones, no agent ever sees or hears the details, which helps platforms reduce their PCI DSS compliance scope.

The flow is simple:

Customer calls the merchant’s payment line.

The automated system prompts for payment details (amount, account number, card info).

Customer enters information via keypad or voice prompt.

Payment processes in real time.

Customer receives instant confirmation.

The entire interaction runs through your SaaS platform’s payment infrastructure, with IVR calling your existing APIs to validate accounts and retrieve balances, and uses the same Payabli APIs, reporting dashboard, and compliance standards as your other payment channels.

How do IVR call trees work for vertical SaaS?

A call tree is the branching logic that guides customers through the IVR payment experience. It’s like a flowchart for phone interactions where each prompt leads to different paths based on what the customer selects.

IVR Call Tree Options

Call trees can be simple (straight to payment) or complex (account lookup, payment options, balance inquiries). The good news? With Payabli, you have options:

Whichever path fits, most platforms go live in weeks, not months. And for teams that want to skip code entirely, Payabli Creator handles it.

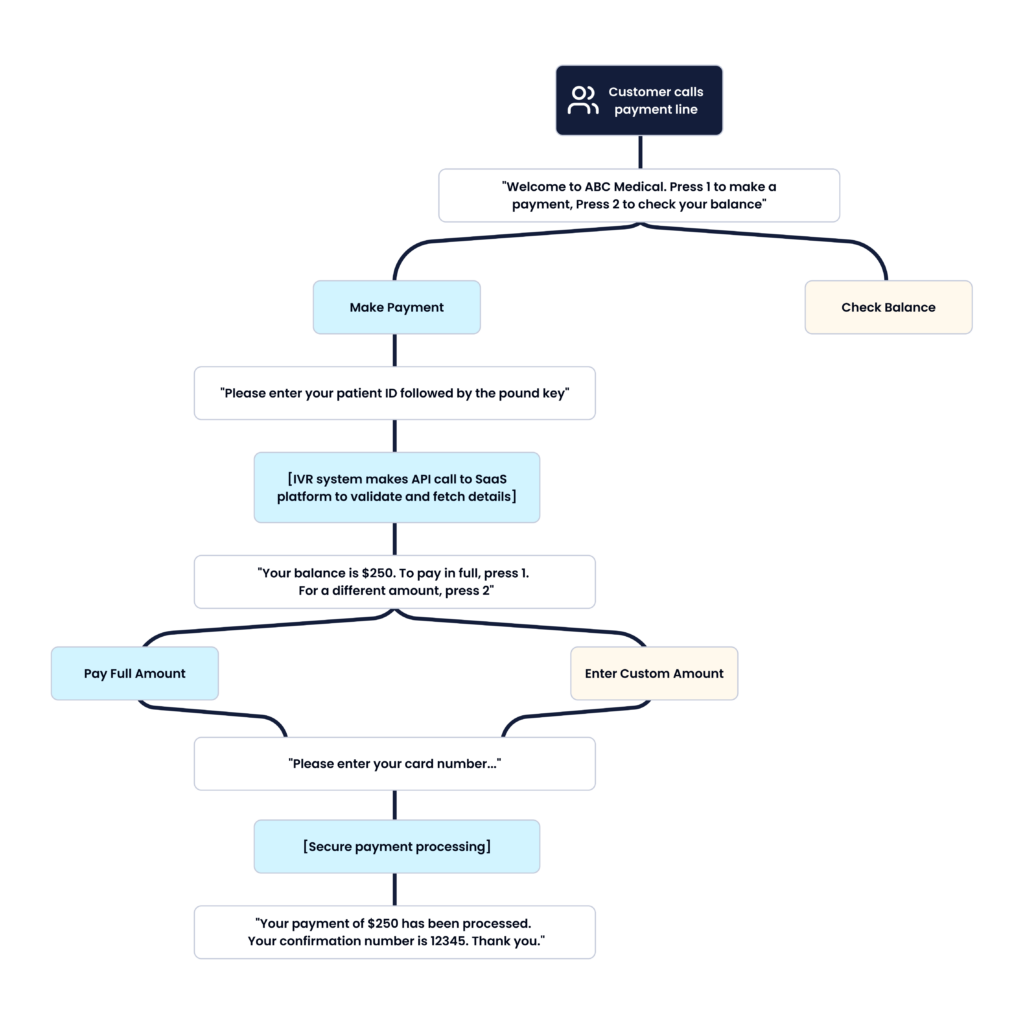

Example IVR call tree for a medical practice

The beauty of IVR call trees is their flexibility. They adapt to your merchants’ specific workflows, terminology, and customer needs. Here’s an example:

Why do IVR payments matter for vertical SaaS?

Adding IVR to your embedded payments offering is not just about giving merchants another channel. It drives measurable impact across revenue, retention, and operational efficiency.

1. Create a new revenue stream

IVR transactions generate higher margins than standard payment processing. You set the service fees (typically per transaction fee, monthly platform fee per phone number, or both) and capture that revenue directly.

These fees are easy to justify with immediate merchant ROI:

Eliminate staff costs for manually processing phone payments

Reduce support calls by 20-30%

Provide 24/7 payment acceptance without adding headcount

Accelerate collections and improve cash flow

2. Deploy quickly without engineering burden

IVR integrates through the same Payabli API as your other payment channels. No separate phone system builds, no phone provider registrations, and no ongoing maintenance teams. Payabli provides a complete, production-ready solution so you can focus on your core product.

3. Create switching barriers

Merchants using multiple payment channels through your platform are exponentially stickier. When you’ve automated their phone payments and integrated with their workflows through your software, switching costs skyrocket. Companies with strong omnichannel customer engagement strategies retain89% of their customers on average, compared to 33% for companies with weak engagement.

4. Unlock high-value vertical use cases

Payabli’s configurable IVR integration enables powerful automation across need-to-pay verticals:

Streamline invoice collection: Law firms let clients pay retainers and outstanding invoices immediately without waiting for mailed checks.

On-time payments: Homeowners and renters can pay HOA dues or rent by phone from anywhere, making it easier to submit payment before the due date and avoid late fees.

After-hours revenue: Field services can capture payment immediately when jobs finish outside business hours.

Self-service payments: Healthcare practices and service businesses let customers pay invoices on their schedule without waiting on hold.

24/7 availability: Emergency services for urgent situations are available anytime without requiring staff.

Why vertical SaaS platforms choose Payabli for IVR payments

In competitive vertical SaaS markets, success means understanding your merchants’ complete operational reality. IVR payments are not legacy technology. They are incremental revenue, reduced churn, and platform differentiation rolled into one capability.

The vertical SaaS platforms dominating embedded payments are not the ones with the flashiest checkout. They are the ones comprehensively solving how money moves 24/7 across every channel. Payabli’s unified payment infrastructure covers payment acceptance, accounts payable, and payment operations, giving you everything you need to be that platform.

Want to add IVR payments to your platform? Book a demo and we’ll walk you through it.