By Emi Keshler | Director of Partner Development at Payabli

I spent the better part of a decade in vertical software startups. Small teams, scrappy budgets, and a payments operation that was usually one person’s problem – mine.

I’ve been the one fielding 2am “fire alarm” calls. I’ve negotiated seven-figure payments contracts. I’ve handled activation rates, merchant onboarding, KYC escalations, chargeback disputes, and compliance audits – often as the only person in the entire company who understood why any of it mattered. I’ve supported, organized, scaled, innovated, optimized, strategized, documented, and implemented. And I did most of it while flying blind.

I am, without question, a payments industry lifer.

But here’s what I’ve learned from all of it: you don’t have to be.

If you’re ready to unlock the real power of embedded payments in vertical SaaS – and you’ve been looking for someone to hand you a map – allow me the pleasure of introducing Payabli’s Partner Development Program.

Why Partner Development Exists

Here’s a scenario I’ve lived through more times than I can count.

When something breaks in your payments program – activation rates drop, a cohort of merchants stalls in KYC, a competitor is undercutting your pricing – who’s responding? If the honest answer is “whoever has the most bandwidth right now,” you don’t have a payments program – you have a payments feature holding on by a thread.

What you actually need is a Head of Payments (HOP). Whether the title is VP of Payments, GM of Fintech, or Payment Operations Manager – the role is the same. It’s the person who already knows what’s wrong before you call them. Who’s already looked around every corner, built a payments strategy, and is ready to move. Research consistently shows that a dedicated subject matter expert is the strongest predictor of successful payments outcomes.

But what if you don’t have that person in-house (yet?) That’s exactly why Payabli built our Partner Development Program.

What Does Partner Development Do?

Think of us as your embedded strategic payments partner – like a fractional Head of Payments who already knows your business. We put on the “Head of Payments hat” and lock arms with you to build a best-in-class payments program from the ground up. Here’s what that looks like in practice:

We start with an honest assessment of your payments program stands today and set clear goals for where you want it to go. Within 48 hours you’ll receive a full strategy and action plan with projected outcomes in 6, 9, or 12 months.

From there, we work alongside you through every phase:

- Evaluation & Goal Setting – understanding your current state and defining what success looks like

- Gap Analysis & Strategy – a comprehensive look at where you’re leaving revenue, efficiency, or merchant experience on the table

- Weekly & Milestone Check-Ins – ongoing accountability and course correction as you grow

- Strategy Execution Tools – hands-on training, custom white-labeled collateral, reporting, business case support, and more

- Optional Co-branded Marketing – showcasing your competitive growth to your own customers and prospects

This is not consulting in the traditional sense. There are no billed hours or recommendations without a shared stake. We’re in the weeds with you – reviewing your merchant lifecycle, diagnosing underperformance, and staying accountable to outcomes for months.

Our gap analysis is comprehensively supportive of immediate results, plus long-term scalability. Examples include:

- Sales: Positioning, talk tracks, incentive structures, negotiation levers, and value-selling training so your team actually knows how to sell payments.

- Merchant Onboarding: Reducing friction from first touch to activation through KYC/KYB education, completion rate optimization, and follow-up sequencing

- People & Support: Tier 1 and Tier 2 support protocols, payments training, emergency preparedness, hiring tips, and the tools your team needs to diagnose and resolve issues fast

- Reporting & Analytics: KPI frameworks, data monitoring, quality control, underperformance diagnostics, and reconciliation to keep your program healthy and accountable

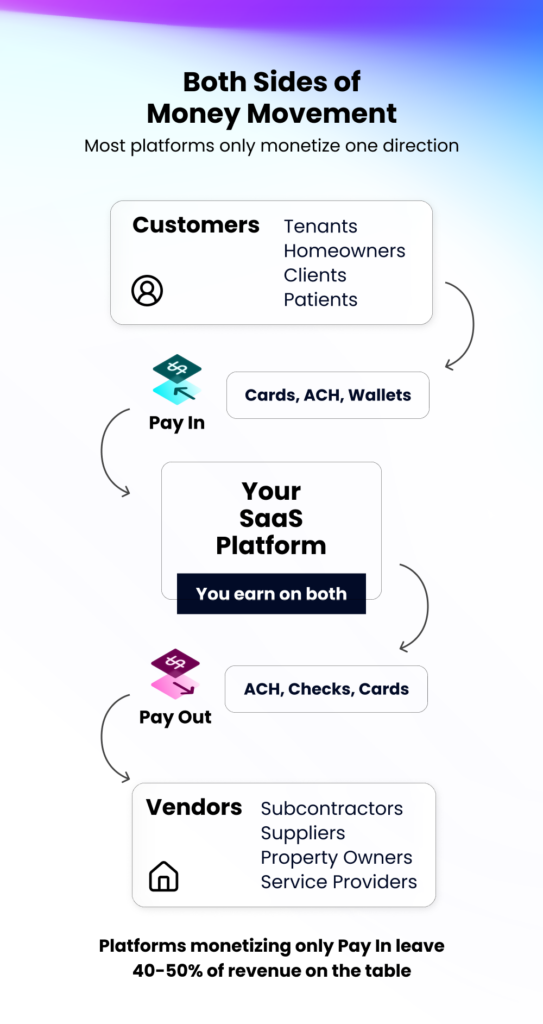

- Merchant Experience: Competitive analysis, product prioritization, vertical-specific optimization, business case development, and the full Payabli Pay In, Pay Out, and Pay Ops framework

- Account Management: Retention, renewals, feature adoption, QBRs, and performance monitoring to protect and grow revenue over time

- Risk & Compliance: PCI best practices, chargeback protocol, Nacha compliance, and merchant offboarding done right

The Partner Development team has spent years solving these problems the hard way – trial, error, and a lot of late nights. We didn’t always have the answers. But we always found them. Now that experience lives in a playbook, and it was made for you.

Come Grow With Us

We are so excited to formally launch our Partner Development Program – and the results from our early partners speak for themselves. They’re growing faster, activating merchants more quickly, and preventing churn before it starts.

If you’re a software operator who has ever stared down a room full of salespeople who didn’t care about payments, scrambled to explain what a good activation rate even looks like, or just wished you had a payments expert in your corner who understands your vertical – that’s exactly who we built this for.

Your payments program deserves more than bandwidth. Let’s give it a strategy.

Emi Keshler is the Director of Partner Development at Payabli. After 7 dog years in the vertical startup world, she joins Payabli to build Partner Development as a dedicated line of business.