Key takeaways

- Intelligent ACH uses machine learning to predict which ACH transactions are likely to return before they are submitted, so a platform can act in advance (adjust timing, reach out, or offer a card) instead of reacting to returns after they land.

- Prediction draws on customer history, account and transaction details, merchant patterns, cohort behavior, and external signals.

- A return probability score can drive real actions: timing optimization, pre-transaction outreach, method routing, retry preparation, reserve management, fraud checks, and capacity planning.

- The limits are real: predictions are probabilities rather than certainties, models drift over time, new customers offer little signal, and prediction-driven actions carry compliance and customer-experience considerations.

- Property management, subscription, and B2B subscription gain the most, while government and utilities gain the least because return rates are already low.

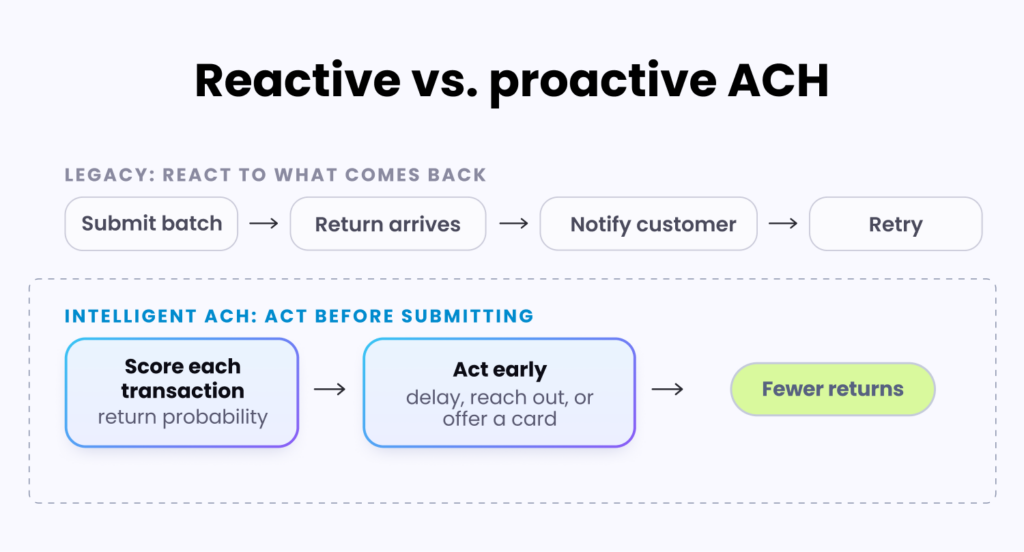

A property management platform runs its rent batch on the 1st. Some of those transactions will come back: insufficient funds, closed accounts, the usual mix. The problem is timing. The platform only learns which ones failed after they fail. The R01 lands on day 3, the tenant gets a notice, and the retry kicks in. Routine, but always a step behind.

Intelligent ACH changes the order of operations. Instead of reacting to returns, a machine learning model scores each transaction before it is submitted, using the end customer’s own history to estimate how likely it is to come back. A tenant with 4 R01 returns in the past 6 months and a pattern of late payments gets flagged before the batch goes out, and the platform can act: delay this submission a few days, reach out first, offer a card for this cycle, or simply staff up for the returns it already knows are coming.

What does intelligent ACH actually mean?

Intelligent ACH is what you get when machine learning sits on top of ACH operations instead of the old habit of submitting a batch and dealing with whatever bounces. The foundation is return prediction: for any given transaction, a model estimates how likely it is to come back, reading the end customer’s history, the account, the transaction details, and the patterns around them.

The rest builds on that one prediction, starting with optimal retry timing, which uses the same signal to pick the day a retry actually clears for a given end customer, learned from their pay cycle. Transaction-level risk scoring folds return probability with fraud and dispute signals so a single number reflects real exposure, and automated routing acts on that number, pushing clean transactions straight through, sending the questionable ones for extra verification, and holding the rest.

Above the level of a single transaction, pattern detection watches whole populations and catches systemic problems a per-transaction score would miss, like a jump in returns across one bank’s end customers that usually means something changed on the bank’s side. Anomaly detection runs the other way, flagging the transaction that breaks an end customer’s or software customer’s normal pattern before it becomes a fraud loss or an operations headache. Together, they change the job from cleaning up returns after they land to heading them off.

What signals predict ACH returns?

ML models for return prediction draw on a wide range of signals. The most informative fall into a few groups.

End customer-level historical signals

An end customer’s own track record is the most predictive thing a model has. The clearest tell is how often they’ve returned before: someone with a string of past returns is far more likely to do it again than someone with a clean record, and a return from three days ago says more about current risk than one from eighteen months back. The return codes matter as much as the count, because a history of R01s (insufficient funds) points to a different kind of future risk than a history of R02s (account closures). Timing and amount fill in the rest. Most end customers pay reliably at a particular point in the month, so a charge that lands off that rhythm carries more risk, and size matters on its own, since the same end customer who clears a $500 debit every time can still bounce a $2,000 one.

End customer-level static signals

Some of what predicts a return never changes from one transaction to the next. Account type and account age both set a baseline, since a freshly opened account carries a different risk than one that has been active for years, and the end customer’s bank sets another, because return rates differ from institution to institution for reasons that have nothing to do with the end customer. Where the end customer is located adds a faint signal on top of that.

Transaction-level signals

The transaction itself tells you a lot before it ever leaves the platform. Amount alone shifts the odds even for the same end customer, and when the charge hits (day of the week, day of the month, hour of the day) moves them again. A debit and a credit start from different baselines, each SEC code carries its own return profile, and even the statement descriptor plays a role, because a charge an end customer does not recognize is a charge they are more likely to dispute.

Software customer-level signals

The software customer shapes every transaction underneath it, so its own numbers feed the prediction. A high overall return rate usually points to something structural, either the kind of end customers the software customer attracts or how it runs its billing, and that shows up in every individual score. Vertical sets an expectation on its own, since property management, subscription, and healthcare all return at different rates, and a newer software customer is harder to read than one with years of history behind it.

Cohort-level signals

People acquired through the same channel or sharing a profile tend to return at similar rates, end customers at the same bank shift together when that bank changes systems or gets acquired, and end customers at the same stage of their lifecycle, whether they just signed up or are on their way out, track one another closely. A single end customer with a thin history often inherits the pattern of the cohort they sit in.

External signals

A few forces sit entirely outside the platform and still move the numbers. Broad economic stress, from rising unemployment to regional downturns, nudges return rates up across the board, and the calendar has its own rhythm, with tax season, the holidays, and summer travel each leaving a mark. Bank-level events matter too, because a merger, a core-system migration, or a fraud episode at one institution can push returns higher for every end customer who banks there.

What can platforms do with return predictions?

Having a return probability score for each transaction enables several operational adjustments.

Timing optimization

Many high scores come down to when the transaction is submitted rather than whether the end customer can pay. If an end customer reliably pays around the 5th to 7th, after their pay-cycle deposit lands, submitting on the 1st will likely draw an R01 that clears fine a few days later, so the answer is to hold the transaction until the pay cycle catches up.

Pre-transaction outreach

For a high score, it often pays to contact the end customer before the charge goes out. A short note works: “Your rent payment is scheduled for the 1st, please confirm the account is funded or tell us if you’d rather use another method this month.” That gives them the chance to add funds or switch to a method that will clear, so a likely return becomes a payment instead.

Method routing

For very-high-probability returns on ACH, offer the end customer card payment instead. The transaction is more likely to succeed, even though card processing costs more.

Retry preparation

For transactions predicted to return, queue the retry workflow to start immediately when the return arrives, rather than waiting for the routine workflow to discover it.

Reserve management

For software customers with elevated return predictions, adjust reserve calculations or hold-back policies to reflect the expected return volume.

Software customer relationship management

For software customers with consistently high return predictions, escalate to a relationship review. The software customer may be better served by a different payment plan, different terms, or a different relationship structure.

Fraud detection

For transactions that look anomalous in ways that suggest fraud, such as an amount or timing very different from the end customer’s usual pattern, flag them for additional verification before processing.

Operations capacity planning

For batches with high overall return predictions, make sure the operations team has the capacity to handle the expected workload.

What are the limitations of ACH return prediction? ML-based return prediction has real limits worth understanding:

Probabilities

A high return probability does not mean the transaction will return, only that it is more likely than baseline. Most high-probability transactions still succeed, so decisions based on predictions need to account for that uncertainty.

Causality is hard

Models predict correlations. A transaction predicted to return for insufficient-funds reasons might actually return for account-closed or some other reason. The category of return can be harder to predict than the binary success or failure.

End customer behavior changes

Models trained on historical patterns may not predict well when an end customer’s situation changes, such as a new job or a life event. Recent data weigh more heavily but are not perfect.

Adversarial dynamics

If predictions drive end customer-facing actions, end customers eventually adapt. End customers who get pre-transaction outreach about insufficient funds may resent the implication and switch providers, so the use of predictions needs to consider end customer experience.

Compliance considerations

Decisions based on predictions need to be defensible. Refusing service to end customers based on ML risk scores can raise fair lending and discrimination concerns if not handled carefully.

Cold-start problems

New end customers without history have no individual prediction signal. Models can use cohort and account-level signals, but predictions are weaker.

Cost of false positives

For some interventions, such as offering card payment or delaying submission, the cost of acting on a false positive is low. For others, such as those refusing the transaction, false positives carry real costs.

Model maintenance

A model that predicts well this quarter loses accuracy over the next few as end customers change how they pay, banks adjust how they handle returns, and the wider environment moves. Keeping it accurate means tracking its performance and retraining it on recent data.

How does Payabli support intelligent ACH?

Payabli’s infrastructure is designed around the Intelligent Fintech Operating System (IFOS) positioning, with capabilities that support intelligent ACH workflows:

Comprehensive transaction history

Per Payabli’s TransEvent reference, complete transaction lifecycle data is available, including all return events. This data is the foundation for any prediction model.

End customer record context

Per Payabli’s documentation, end customer (paycustomer) records aggregate the end customer’s transaction history with their characteristics, providing the end customer-level features models need.

Software customer context

Platform-level reporting provides software customer-level features that models can use.

Webhook events for real-time signals

Real-time event data (returns happening, NOCs arriving, transactions completing) flows through webhooks, so models can update with current information.

API access for prediction integration

Platforms with their own ML capabilities can pull data through Payabli’s API, run predictions in their own systems, and use the results to inform processing decisions through the same API.

Built-in intelligent capabilities

Per Payabli’s broader infrastructure positioning, intelligent capabilities such as intelligent funding and intelligent risk monitoring are built into the platform, so platforms can use them without building their own ML infrastructure.

Integration with broader risk infrastructure

Payabli’s risk infrastructure considers prediction signals alongside other risk signals such as fraud detection and compliance monitoring for coherent decision-making.

Should you build or buy an intelligent ACH? For platforms considering an intelligent ACH capability, the question of whether to build their own or use Payabli’s matters.

Factor Build your own Use Payabli’s infrastructure

What it takes ML expertise, data infrastructure, ongoing model maintenance, and integration with operational workflows Minimal beyond standard Payabli integration What you get Full control and customization Built-in intelligence applied across all transactions, improving as Payabli’s models evolve best for platforms with sophisticated ML capability and very specific customization needs Most platforms, especially those without ML expertise as a core capability Investment Substantial: data scientists, ML engineers, infrastructure, and ongoing operational resources Minimal

For most platforms, using Payabli is the right answer. A platform’s ML investment is better spent on differentiating product features than on intelligent ACH, which Payabli does for them.

Which verticals benefit most from intelligent ACH? Different verticals get different values from intelligent ACH.

Vertical Value

Different verticals have different value from intelligent ACH.

Property management has high value from prediction. Tenant payment patterns are reasonably predictable, R01 returns are common and recoverable, and operational adjustments based on predictions can substantially reduce return rates.

Trade services have moderate value. Customer base is more variable; predictions are less stable. Specific use cases (large project payments) benefit from prediction.

Healthcare has moderate value. Patient payment patterns vary widely; predictions provide modest lift over baseline.

Subscription services have high value. Predictions about likely R10/R11 disputes help target retention efforts and authorization renewal.

Education has high value during tuition cycles when accurate prediction enables proactive outreach.

Government and utilities have low value. Return rates are already low; marginal improvement is small.

B2B subscription has high value due to high transaction values where prediction-based interventions have substantial economic impact.

Identify high-value scenarios

Find where prediction provides the most value, usually high-volume software customers with elevated return rates and the operational capacity to act on predictions.

Pilot with limited scope

Start with one software customer or one end customer cohort. Apply predictions, take operational action, and measure outcomes against control groups that do not get the intervention.

Refine and expand Based on pilot results, refine the approach and expand to more software customers or end customer segments.

Operationalize

Build the intervention into the standard workflow rather than treating it as a special program. Ongoing measurement ensures it continues to provide value.

Continuously improve ML models and the operational responses around them benefit from periodic review and refinement, which keep the capability valuable.

The bottom line ACH return prediction is becoming a real capability. The platforms that integrate it thoughtfully into their operations capture meaningful efficiency gains and improved software customer outcomes. The platforms that ignore it operate at a growing disadvantage as competitors take advantage of intelligent operations. Working with infrastructure that has intelligence built in lets platforms benefit from the capability without making the substantial ML investment that building their own would require.

If you are a software company, you are a payments company.

Book a demo to see how Payabli’s infrastructure supports intelligent ACH for your platform.