Key takeaways

- Agentic payments let an AI agent pay vendors on a business’s behalf, reading the context behind a bill, choosing the rail, and releasing payment within set limits while the rails execute under fixed controls.

- The real change is who decides, not how fast money moves. A rule is set ahead of time, and an agent reasons at the moment of payment.

- An agent pays in four stages: detect, evaluate, route, and reconcile, with most of the judgment and risk in the middle two.

- Safety comes from limits that the agent cannot lift, a fixed list of who it may pay, single-use credentials, and a record no one can alter after the fact.

- Agentic payout lands first in service businesses, field service, construction, healthcare, and the like, where paying vendors is constant and rule-bound.

- The agent is only as capable as the platform under it, and that infrastructure is live on Payabli today.

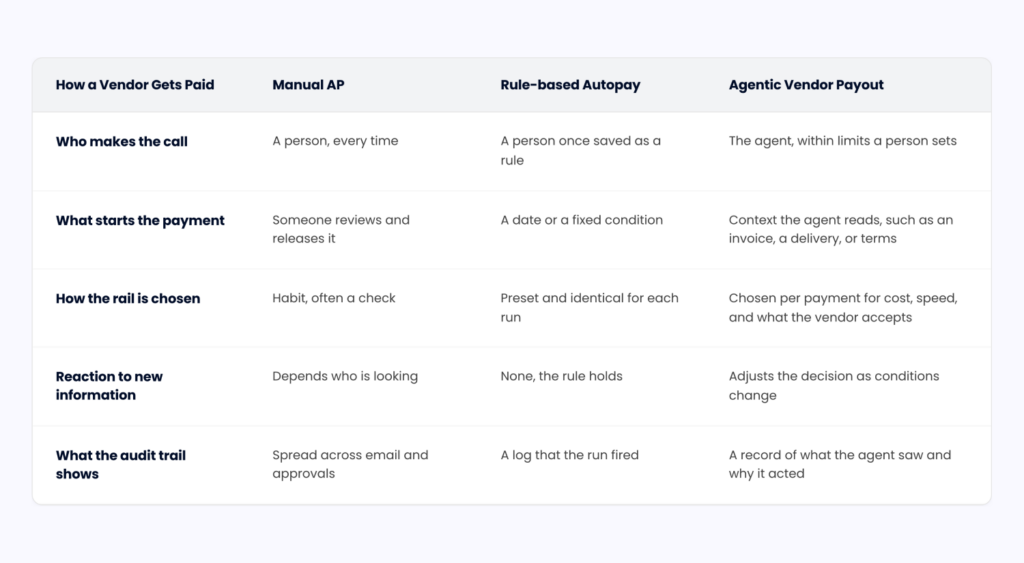

Paying a vendor still usually starts with a human decision. Someone confirms whether the vendor takes a card, finds the right remit details, and when that drags on, defaults to a check. Checks still made up 26% of B2B payments in 2025. Agentic payments move that decision to software. AI agents are starting to read the context of an invoice and execute the payout within rules a business sets, and for platforms whose merchants run accounts payable, that shift lands on the infrastructure underneath them.

How are agentic payments different from automated payments?

Most platforms already move money for their merchants without a person pressing send. Recurring billing runs on a schedule. A vendor invoice clears on its due date. An ACH batch goes out every week like clockwork. That is automation, and accounts payable has leaned on it for a long time.

Agentic payments are not a faster version of that. What changes is where the decision sits. An automated payment carries out a choice a person has already made and saved as a rule. An agent makes the choice in the moment, then acts on it.

That sounds like a small shift. It is not.

Payment rails are built to be deterministic, which means a rule runs, the result is fixed, and once funds settle, the payment is final. AI agents work the other way, weighing changing information and landing on a judgment rather than a guaranteed outcome. In an April 2026 note, the International Monetary Fund framed the central problem as the mismatch between how AI agents reason and how payment systems are built to run.

The implication for anyone building this is direct. An agent can decide what ought to happen, but the rails still have to execute it under controls that do not flex.

Hold that against a single vendor invoice, and the difference is easy to see. A scheduled autopay sends the same amount to the same vendor on the same day, whether or not the invoice matches the original order, and whether or not paying a few days early would capture a discount the business is otherwise leaving behind. It weighs none of it, because nothing in the rule asks it to.

An agent can read the invoice, compare it against the purchase order and the agreed terms, decide whether to pay now or hold, choose the payment method that fits, and release it within the limits the business has set. Automation follows an instruction. An agent forms one.

What matters is no longer whether a payment can be automated. It is what the agent is allowed to decide, and what record it leaves behind. That is where this turns into an infrastructure problem for any platform running payouts for its merchants, and it is what the next section traces in full, from invoice to settled payment, for one vendor.

How does an AI agent pay a vendor?

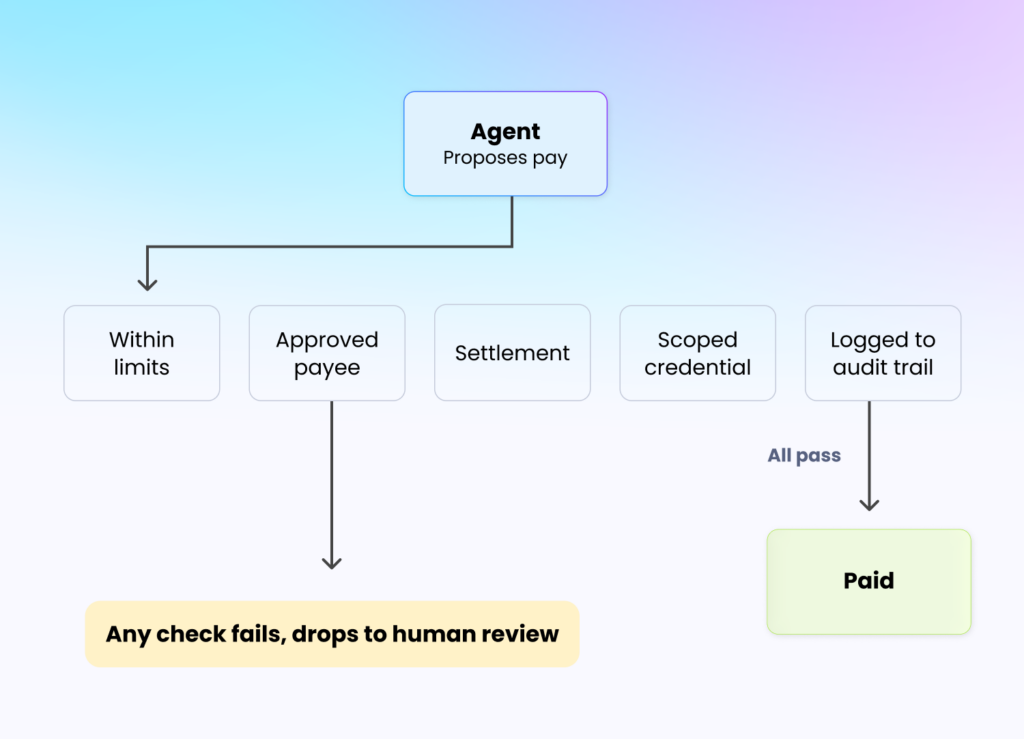

Follow one payment the whole way through. A merchant on your platform owes a vendor, an agent is cleared to handle it, and the work splits into four stages in order. The agent notices the payment is due, works out what the rules permit, moves the money down the right rail, and closes the books. Most of the difficulty, and most of the safety, lies in the two middle stages.

The principle underneath them is simple. Keep the thinking apart from the paying. The agent forms and checks what should happen, the rails settle it, and nothing crosses from decision to execution without passing a control.

-

Trigger detection

A payment starts with a signal, not a calendar. The agent watches the systems a merchant already uses and acts when one of them says a vendor is owed. An invoice lands in the inbox. A job is marked complete in field service software. A delivery is confirmed against a purchase order. A subscription comes up for renewal.

What sets this apart from a scheduled run is that the trigger carries context. The agent sees not just that a payment is due but why, tied to the document or event behind it. That context is the raw material for every decision that follows, and the reason the same vendor can be paid differently from one month to the next.

-

Context and policy evaluation

Most of the judgment happens at this stage. Before anything moves, the agent builds the full picture and tests it against the rules the business has set.

It reads the invoice alongside the purchase order, the agreed terms, the vendor record, and the merchant’s current position, then runs the checks a careful AP person would. Does the invoice match the order? Is the amount within the limit for this vendor? Has it already been paid? Does anything look off? Would paying early earn a discount worth taking?

This stage is also where authority gets proven, not assumed. Standards are forming around exactly this point. The Agent Payments Protocol, an open standard Google launched in September 2025 with more than 60 payments and technology organizations, uses signed mandates that record what an agent was permitted to do, so a payment traces back to a pre-approved instruction rather than a guess. Fail a check, and the payment does not proceed. It stops, or it routes to a person.

-

Payment routing and execution

Once a payment clears, the agent moves it, and the method is a decision rather than a default. It weighs cost, speed, and what the vendor accepts, then picks the rail. Same-day ACH for something time-sensitive. A virtual card where the vendor takes cards, and the discount or protection is worth it. Standard ACH where neither speed nor incentive changes the math.

The execution stays deterministic, and that matters. The agent decides what should happen, but the rail carries it out exactly as instructed, with no room to reinterpret the amount or the recipient. That is what keeps an agent-initiated payment from behaving like a guess with money attached.

-

Reconciliation and audit

The payment is not finished when the funds leave. The agent records it against the right invoice and merchant, updates the books so the entry lands in the correct period, and confirms the vendor was paid. The month-end chore happens at the moment of payment.

The audit trail is what earns trust. A complete record shows what the agent saw, which rule it applied, why it paid, and which rail it used. For a platform answering to merchants, sponsor banks, and auditors, that trail is what makes letting an agent move money defensible. But a record only proves what happened after the fact. Stopping the wrong payment before it leaves takes a different set of controls.

What guardrails make agentic vendor payments safe

An agent should never be trusted because it is capable. It should be trusted because it cannot exceed what it was allowed to do. That idea follows straight from the split we drew earlier. The agent’s judgment sits on one side, the controls sit on the other, and the controls are not advice that the agent can choose to ignore. They are enforced by the infrastructure beneath it.

Four controls do most of the work, and each answers a different question. How much can move, to whom, with what credentials, and with what record left behind.

-

Spending limits and velocity controls

The first thing to bound is how much an agent can move and how fast. The caution is earned. In a 2026 Cloud Security Alliance survey, nearly two in three organizations had an AI-agent incident in the prior year, and 35% of those caused financial loss. An agent that misreads context or gets manipulated does not pause to reconsider. It fails at machine speed.

So the limits sit below the agent and are enforced at the rail, not at the model’s discretion. Per-transaction caps. Daily and monthly ceilings. Velocity limits that catch an unusual run of payments to the same place. Cumulative thresholds that flag when a period’s spending nears its budget. The controls work best when they are risk-proportional, so a small recurring software payment clears on its own while a first-time five-figure payout to a new vendor meets a tighter limit or stops for a person.

-

Approved-payee enforcement

Bounding the amount means little if the money can still reach the wrong place. The more dangerous question is to whom.

This is where the real fraud lives. The FBI’s Internet Crime Complaint Center logged $2.77 billion in business email compromise losses across 21,442 complaints in 2024, the scam that redirects a routine-looking vendor payment to an account the attacker controls. An agent that can pay anyone is the same risk with the brakes off. The fix is to let the agent pay only payees that have already been verified and approved. A new payee, or a change to an existing one’s bank details, drops out of the automated path and into a separate review. The agent can put a payment forward, but it only goes through if the payee is already approved.

-

Tokenized, scoped credentials

Even if bound and aimed correctly, an agent should never hold a reusable payment credential. Tokenization already swaps the underlying account detail for a stand-in, so the real number never sits in the agent’s hands. Scoping takes it further by tying that stand-in to a single use, one payee, one amount, a narrow window of time.

This is the least privilege applied to money. OWASP, in its guidance on agent risks, puts it plainly and recommends you limit an agent’s permissions to the minimum necessary so the scope of any undesirable action stays small. A credential that can do exactly one thing cannot be repurposed into something else, even if the agent is compromised or confused.

-

Audit trails for every agent action

The first three controls decide what an agent can do. The audit trail is how you answer for what it did.

The workflow already produces a record of each payment. What turns that record into a guardrail is that it cannot be quietly changed afterward. An append-only, tamper-evident log is the difference between a story that can be rewritten and evidence that holds. The reason this matters is accountability. As the NIST AI Risk Management Framework puts it, accountability presupposes transparency. When a merchant, a sponsor bank, or an auditor asks why a payment happened, the answer has to be retrievable and trustworthy. When an agent acts, a person or a business is still answerable for it, and a tamper-evident trail is what makes that responsibility enforceable rather than theoretical.

Taken together, these four controls are less about restraining the agent and more about what the platform underneath it has to enforce. Where that enforcement gets put to work first is not where most of the coverage is looking.

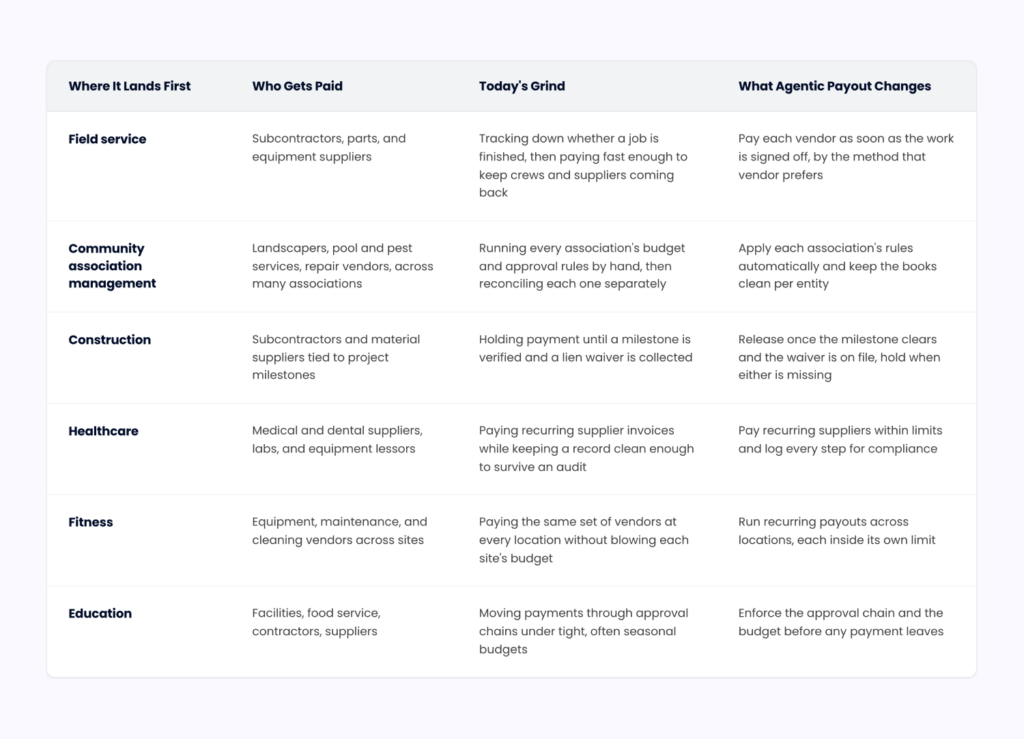

Where agentic payments are landing first in need-to-pay verticals

Most stories about agentic payments picture a shopper’s assistant buying something at checkout. That is not where this lands first. It goes to the service businesses that pay vendors to operate, the kind that treat accounts payable as a standing weekly job, not an occasional errand. The pattern is clearest in six of them:

- Field service

- Community association management

- Construction

- Healthcare

- Fitness

- Education

Start with why these businesses and not, say, a clothing store. In a service business, paying vendors is not back-office housekeeping. It is the operation itself. The work is not finished until the people who did it are paid, and what comes next waits on that payment clearing. These payouts also have a shape that an agent is built for. They recur on a known cadence, they follow rules the business already set, and the volume outpaces whatever one person can stay ahead of. Routine but high-stakes, rule-bound but constant, it is the work that wears a person down and the kind of work an agent can carry.

A retailer does not live here. A store mostly takes money in at a counter or a checkout page. These verticals run the other direction. They stay open by pushing a steady stream of payments back out to the vendors that keep them running, and that outbound stream is where an agent earns its place first.

What that looks like, vendor by vendor, is below.

Some of this already exists. Before an agent can pay a vendor on its own, something has to work out how that vendor wants to be paid. That part is live today. An agent calls to confirm whether a vendor accepts a card. An invoice is read into a vendor record. A virtual card is sent by email. What is not here yet is the last step, an agent that runs the whole payment on its own without a person. These verticals will get there first, because the pieces that come before the payment already work.

Some of this already exists. Before an agent can pay a vendor on its own, something has to work out how that vendor wants to be paid. That part is live today. An agent calls to confirm whether a vendor accepts a card. An invoice is read into a vendor record. A virtual card is sent by email. What is not here yet is the last step, an agent that runs the whole payment on its own without a person. These verticals will get there first, because the pieces that come before the payment already work.

The thread running through all six is the same. The businesses doing this work do not build payment systems of their own. They run on a platform that hands them one. So whether agentic payout actually reaches a field service company or a property manager comes down to the platform underneath them, and what that platform is able to carry.

What software platforms need to support agentic vendor payments

Walk back through what an agent does to pay a vendor, and what keeps it safe, and the requirements almost write themselves. The agent is the easy part to picture. The infrastructure it stands on is what decides whether a platform can offer agentic payout at all. Five things have to be in place, and Payabli runs all five today.

What agentic payout needs, and what already exists

| What the platform must provide | Why the agent needs it | Live on Payabli |

| One connection to every rail | The agent picks the method only if the platform can reach it | Card, ACH, and check across one integration, with RTP and push-to-card coming |

| Verified vendor records | Approved-payee rules are only as good as the records behind them | Human and AI vendor enablement, automated vendor and merchant enrichment, OCR invoice capture, and payment matching |

| Controls the platform enforces | Limits and approvals belong in the platform, not the agent’s judgment | Spend-limit rules, approval workflows, ML, and heuristic risk screening |

| A record that cannot be edited | Accountability depends on a trail no one can quietly change | Full-lifecycle payment audit trail, reconciliation, and reduced PCI scope |

| Structure for many entities | Multi-association and multi-location books cannot be shared | Unlimited parent-child architecture |

None of this is hypothetical. It is the payout infrastructure Payabli runs now, on one set of payment functions across Pay In, Pay Out, and Pay Ops. The autonomous agent that completes a payment on its own is the part still arriving, and when it does, it will not need a new stack. It runs on the one a platform already has.

So the question stops being whether you can build for agentic payments. It becomes how soon you want to turn it on. Book a demo to see the payout stack it would run on.

Frequently asked questions

- What is the difference between agentic payments and agentic commerce?

The useful split is focus. Agentic commerce is the buying side, an AI agent finding a product or service and completing a purchase. Agentic payments are the money-movement layer underneath it. This article covers one direction of that layer, vendor payout, where an agent pays the suppliers and subcontractors that a business depends on, rather than buying anything for it. The acceptance side, where an agent initiates a payment that a merchant receives, is its own topic. -

What payment rails do AI agents use to pay vendors?

The same rails any business already uses. There is no special agent rail. An agent pays over ACH and same-day ACH, a card or virtual card, a paper check, or a real-time rail like RTP or FedNow. What is new is that the agent picks among them per payment instead of defaulting to one. And despite coverage that frames agentic payments around stablecoins, vendor payout in service businesses runs on these everyday rails, not crypto.

-

How do platforms protect merchants from runaway AI agent spending?

The safeguards assume the agent might misfire, so they do not depend on it behaving well. Spending authority is set as fixed limits enforced outside the agent, so a sudden burst of payments or a climb past a budget ceiling puts a halt rather than continuing. Anything over the line pauses for a person. The worst a malfunctioning agent can do is bound in advance.