Key takeaways

- Retention in vertical SaaS is rarely a feature problem. It’s a payments problem: when merchants manage money outside your platform, your software becomes optional.

- The retention benefit comes from both sides of money movement: Pay In (payment acceptance) on the inbound side and Pay Out (accounts payable disbursements) on the outbound side.

- Embedding payments into a platform’s daily workflow, not just adding it as a feature, is what turns software into infrastructure merchants can’t easily replace.

- Fintech-led vertical SaaS platforms have the strongest retention profile in software. A 5% lift in retention can boost profits 25% to 95%, according to Bain & Company.

- The most common mistakes: low payment adoption, payments running outside the product, and onboarding that never gets merchants to their first transaction.

The average B2B SaaS platform loses about 4.2% of its customers every year. Most operators respond the way the playbook says to: better support, more features, sharper pricing. Those things help at the margins. But for vertical SaaS platforms, the biggest lever on retention isn’t any of them. It’s whether your merchants run their money through your platform or around it.

Why retention is harder than most vertical SaaS operators expect

In need-to-pay verticals, the merchants who churn aren’t usually the ones who complained. They’re the ones who quietly kept processing payments outside your product until switching cost them nothing.

A few patterns show up again and again:

Fragmented payment management. A platform handles operations well but leaves payments to outside tools. Every transaction processed elsewhere is one more reason for a merchant to log into another tool, and one more reason to eventually leave for it.

Payment friction, not software gaps. In property management, construction, and field services, the trigger for churn is often the payment experience, not the core product. A merchant who can’t collect efficiently through a platform will find one that lets them.

Onboarding that never activates the financial workflow. Merchants who don’t start using payments in their first few weeks rarely pick it up later. Onboarding decides whether a merchant builds real dependency on a platform or stays on the surface.

Outbound payments nobody is watching. Most platforms track money coming in. Far fewer track money going out. When merchants pay vendors through outside systems, that’s a daily workflow the platform doesn’t own.

Growth that outpaces retention. Adding merchants without deepening payment adoption keeps churn high no matter how fast a platform grows, and acquiring a new merchant costs far more than keeping one.

How does embedded finance improve customer retention for SaaS?

Embedded payments infrastructure addresses each of these challenges at the infrastructure level, not the feature level. Most platforms try to solve retention through better support or more features. Neither works if your merchants are running their financial workflow elsewhere. Each solution below maps directly to a challenge above, because fixing retention means owning the layer merchants depend on to move money.

How does centralizing payments inside a SaaS platform reduce churn? When Pay In (payment acceptance), Pay Out (vendor payouts and accounts payable disbursements), and Pay Ops (reconciliation and payment operations) all run inside your product, your merchants stop splitting their workflow across tools. Your platform becomes the operational center, not one of several. That is when your platform stops feeling like software and starts feeling like the way they run their business.

How does embedded finance eliminate payment friction for merchants? In construction with progress billing or property management with ACH rent collection, removing payment friction matters more than any feature update. When your merchants can collect, invoice, and pay vendors without leaving your platform, there is no reason to look elsewhere.

Why should SaaS platforms embed outbound payments, not just inbound? Embedding Pay Out or accounts payable disbursements — means your merchants’ vendor payments run through your platform too. Merchants running both sides through your product have no financial workflow left to manage elsewhere. If you overlook outbound, you are leaving both retention and revenue on the table.

How does embedded finance simplify merchant payment onboarding? The faster a merchant processes their first payment through your platform, the more likely they are to stay. Frictionless onboarding built into your payment operations gets merchants to that moment faster. Use the embedded payments launch checklist to map the steps that cut early churn.

How do embedded financial features increase platform stickiness? According to BCG, SaaS platforms with embedded payments already account for 36% of SME acquiring revenues, with that share projected to reach 45% by 2028. The more financial workflows your merchants run through your platform, the harder it is to replace you.

Why does embedded finance work well for vertical SaaS?

Embedded payments infrastructure improves retention across SaaS broadly, but the effect is strongest in vertical markets. Generic solutions built for horizontal e-commerce do not map onto the workflows your merchants actually use. And your merchants already trust your platform with their daily operations, which means adoption of embedded finance is faster than it would be on any other platform they use.

Why do vertical SaaS platforms see higher embedded finance adoption? Your merchants already trust your platform with their operations, their customer data, and their daily workflows. Embedded payments introduced into a product they already depend on get adopted faster because the trust is already there. You are not asking them to try something new. You are extending something they cannot afford to lose. Adding embedded payments infrastructure to a vertical SaaS platform can increase revenue per customer by 2 to 5 times. Higher revenue per customer and stronger retention are not separate outcomes. They are the same shift measured two different ways.

Why does generic payment infrastructure hurt retention in vertical SaaS? Generic payment infrastructure is built for horizontal e-commerce, not your merchants’ actual workflows. Property management needs lockbox collections. Construction needs progress payments. Field services need same-day payouts. When your payment infrastructure does not fit those workflows, your merchants build workarounds outside your platform. Every workaround is a workflow you do not own, and every workflow you do not own is a retention risk. Purpose-built payments infrastructure for vertical SaaS removes that friction instead of creating it.

What should SaaS platforms look for in an embedded payments solution?

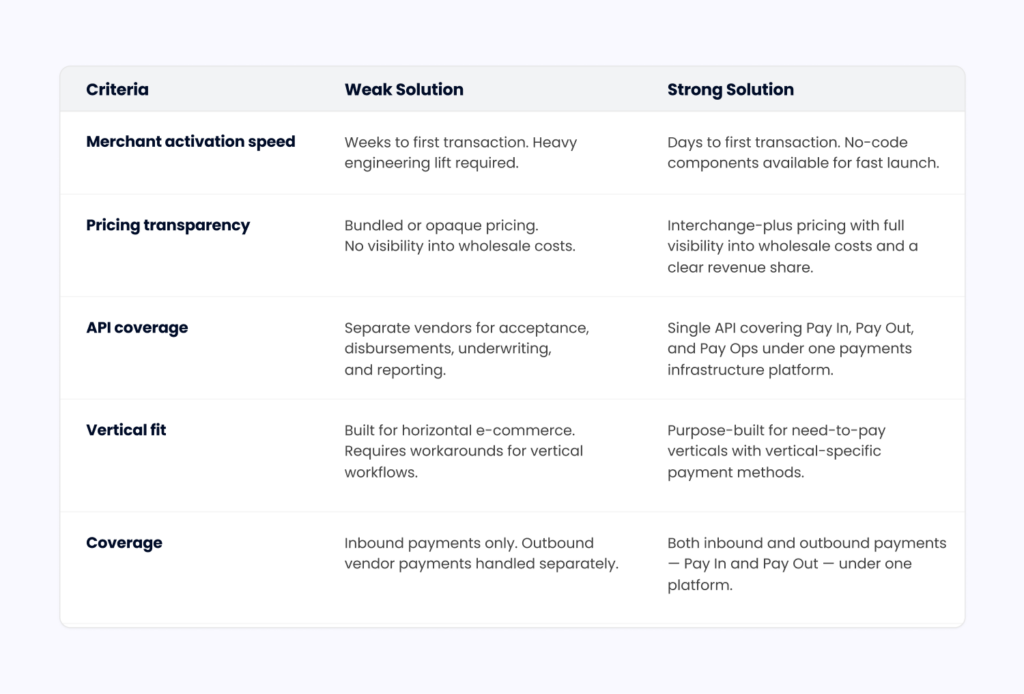

Not every embedded payments solution is built for retention. Some get merchants processing quickly. Others create months of integration work before a single transaction clears. If you are evaluating options for your vertical SaaS platform, these are the three questions that matter most.

How quickly can merchants activate and process their first payment? Activation speed is a retention metric, not an implementation one. Every day between integration and the first transaction is a day your merchant has not built dependency on your platform. The right solution gets merchants live in days, not weeks, with no-code embedded components that do not require a full engineering sprint.

Is payment pricing transparent with a clear revenue share model? If you cannot see your wholesale interchange costs, you cannot protect your margin. The right solution shows you exactly what you are paying, what your merchants are paying, and what you keep. Interchange-plus pricing is the only model that gives you that visibility.

Does it offer a single API, or does it require managing multiple vendors? Every vendor you add to your payment stack creates more friction for your merchants and more blind spots in your data. Separate tools for Pay In, Pay Out, and Pay Ops mean your payments business is spread across systems that do not talk to each other. A single API that covers payment acceptance, accounts payable disbursements, and payment operations keeps everything in one place.

The table below shows what these criteria look like in practice across a weak solution and a strong one.

How can Payabli boost customer retention for SaaS platforms?

Payabli gives vertical SaaS platforms a single embedded payments infrastructure covering Pay In, Pay Out, and Pay Ops, so your platform earns on both sides of money movement while deepening merchant dependency.

ExactEstate, a property management SaaS platform, saved its clients up to $1M annually in payment fees after consolidating onto Payabli. That cost reduction removed the payment friction that was quietly driving merchants to look elsewhere. Merchants who save money and simplify operations through your platform do not look for alternatives.

Every transaction your merchants are processing outside your product today is a retention risk you can close. Payabli exists to help you close it.

Book a demo to see how it applies to your vertical.