Key Takeaways:

- The best practice to embed payments in SaaS is to find an infrastructure partner that unifies payment acceptance, disbursements, and operations within a single API, with seamless merchant onboarding, white-labeled user experience, and a scalable pricing strategy.

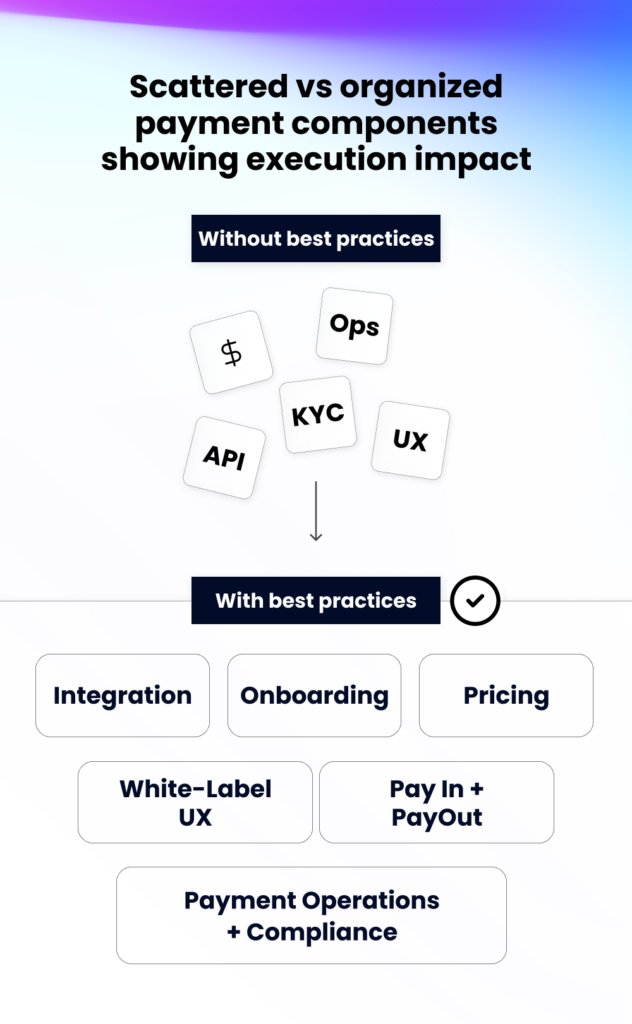

- The three essential decisions include merchant onboarding flow, integration model (API, no-code, or white-label), and the pricing model. Missteps in any of these would delay adoption.

- White-labeling the entire payment workflow keeps merchants inside your platform, resulting in reduced churn rate and driving higher payment adoption rates.

- Payment operations (onboarding, compliance, risk, billing) are just as important as the payment technology; however, 70% of the platforms still treat payments as a commodity.

- SaaS platforms that combine acceptance, disbursement, and operations under a single API eradicate vendor fragmentation and go live in weeks instead of quarters.

Embedding payments in SaaS is one of the most consequential decisions a software platform can make — and one of the most misunderstood. The technical lift of adding a payments layer is only part of the equation; the real complexity lies in architecting an experience that drives merchant adoption, scales with your business, and captures the full revenue potential payments can unlock. Platforms that treat embedded payments as a feature rather than a strategic capability often find themselves rebuilding from scratch. Getting it right the first time requires a clear-eyed understanding of where the pitfalls are — and how to avoid them.

Meanwhile, platforms that follow proven implementation strategies are doubling their payments revenue within three months of launch (EY-Parthenon). The gap between doing it and doing it well is worth millions, as it is projected that with embedded payments transaction value would surpass $2.5 trillion by 2028 (Juniper Research). This guide covers eight best practices that distinguish platforms generating real payment revenue from those still figuring it out.

1. Choose the Right Integration Approach

There are three paths to embedding payments, each with different tradeoffs around control, speed, and engineering lift.

- Pre-Built Payments Portal: The fastest entry point. Payabli’s ready-made portal and hosted tools let you start accepting and managing payments without building much yourself. Payments are functional from day one, with white-label opportunities to keep it on-brand.

- Embedded Components: Pre-built JavaScript UI modules (payment forms, boarding links, merchant dashboards) that drop into your platform with minimal development effort. Launch in weeks with full functionality and CSS-level branding control. This is where most SaaS platforms land when they want payments inside their product without heavy infrastructure work.

- Full API: Complete control over every screen, data point, and workflow. The right choice for platforms with dedicated engineering teams that want a fully tailored payment experience. It takes longer to build, but you own every interaction.

Partners shouldn’t have to start at the most complex integration. Payabli supports a natural progression: launch quickly with hosted tools, embed payments with configurable components, then build a fully custom experience when you’re ready.

2. Make Merchant Onboarding Frictionless

The first experience your customers will have with payments on your platform is merchant onboarding. If the process feels disconnected from your product or adds unnecessary friction, adoption can stall before it even begins.

The most effective onboarding workflows share a few core principles. Use existing platform data — tax ID, business name, address — to pre-fill the merchant application, so customers aren’t re-entering information they’ve already given you. Keep the form completable in a single session. Deliver the experience through a white-labeled boarding workflow so merchants stay within your platform from start to finish. Leverage automated KYC/KYB verification to remove manual bottlenecks, and surface real-time application status updates so merchants always know where they stand — reducing drop-off and accelerating activation.

According to BCG, a higher activation and retention rate is observed on platforms that have seamless onboarding, as it reduces friction in merchant experience.

3. White-label Everything

The payment experience should feel native to your platform. For you and for every merchant you serve. When a merchant onboards, submits a payment, checks a dashboard, or receives a receipt, that interaction is a direct reflection of your product. Friction at any one of those touchpoints isn’t just a UX problem, it’s a retention risk.

Every step should carry your brand: checkout pages, payment forms, reporting dashboards, onboarding applications, transactional receipts, email notifications, and settlement communications. When merchants see consistent branding across every interaction, payments feel like a core feature of your platform — not a third-party service bolted on. That consistency builds trust, drives adoption, and reduces churn.

With more than 60% of vertical SaaS platforms already embedding payments (EY-Parthenon), your merchants expect this level of consistency. The bar for what “native” looks like is only rising.

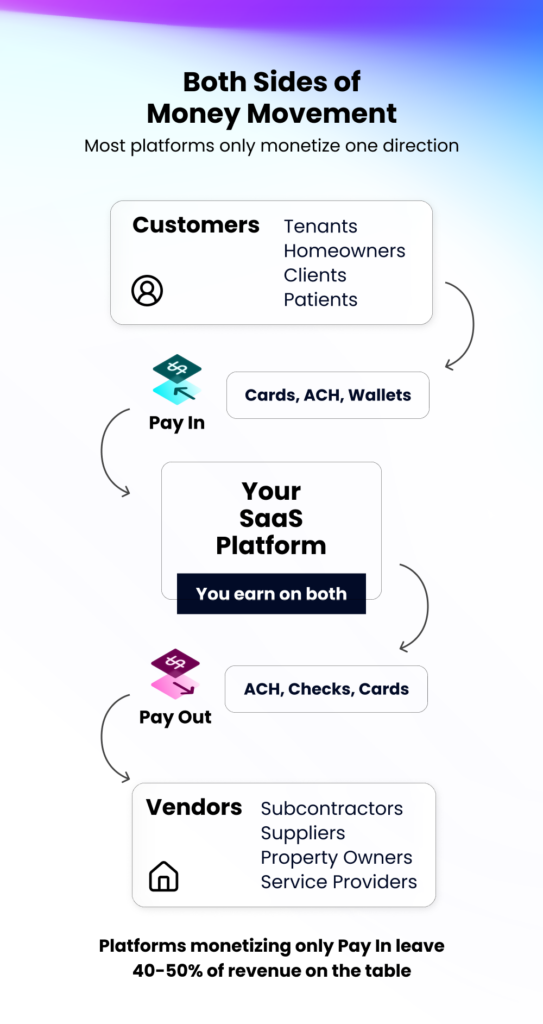

4. Cover Both Sides of Money Movement

Payment acceptance (Pay In) is table stakes for most platforms, but merchants also send money, like paying vendors, suppliers and subcontractors. This is the account payables (Pay Out) option, and it represents a substantial revenue opportunity.

For example, in a construction management platform, a general contractor collects payments from the property owners (Pay In) and then is required to pay plumbers, electricians, and other suppliers (Pay Out). Similarly, in property management, a platform’s client collects rent from tenants, then pays utility companies, maintenance vendors, and property owners. The platforms that only monetize one side of payments are leaving potential revenue on the table, as both sides of the payment carry a margin.

The best practice is to choose a platform with a single unified API offering both acceptance and disbursements. A unified view of all money movement across your platform is enabled, without the need to manage two separate vendors. When Pay In and Pay Out share the same reconciliation, reporting, and billing layer, the operational friction reduces critically.

5. Don’t Ignore Payment Operations

Payment operations are the backbone of a scalable payments strategy — and the most underestimated part of it. Getting live is the easy part. Pay Ops is what ensures merchant underwriting, chargeback management, risk and fraud monitoring, compliance reporting, pricing and billing configuration, and funding and settlement management run efficiently — freeing your team to focus on growth instead of back-office overhead.

Most software platforms treat payments as a utility. The ones that treat it as a strategic lever — investing in the operational layer, not just processing — are the ones that drive retention, unlock new revenue, and build durable competitive advantage.

The takeaway: choose a partner that offers operational depth alongside a payments API, not just processing capability. Onboarding templates, billing engines, risk controls, and reporting dashboards are just as important as accepting a card payment.

6. Offer Multiple Payment Methods

Your merchant’s customers expect multiple payment options at checkout. At minimum, platforms should provide support for credit and debit cards (Visa, Mastercard, Discover, Amex), bank transfer and ACH, digital wallets (Google Pay, Apple Pay), SMS pay links, and checks, such as RDC (remote deposit check capture) for verticals that need it.

Your payment methods should match your vertical. A property management platform needs ACH and remote deposit check capture — how most homeowners and tenants prefer to pay. An education platform benefits from recurring billing and flexible payment schedules. A field service platform needs Tap to Pay and digital wallet support for fast, on-site transactions. And regardless of vertical, any modern payment stack should include digital wallets: Juniper Research cites “global digital wallet users will exceed 5.2 billion by 2026, growing by 35% between 2025 and 2030.”

7. Build a Pricing Strategy That Scales

Instead of simply passing through processing costs, treat payments as a standalone P&L — built to optimize operations, maximize revenue, and scale your business.

Pay In: Your pricing model determines how much of the payments opportunity you capture. IC+, tiered, flat rate, or zero-cost processing — configure the right model for the right customer across your entire portfolio.

Pay Out: Every vendor payment your platform sends is a transaction — and every transaction is a chance to capture margin. Virtual cards generate interchange. ACH can carry per-transaction fees. Checks have issuance economics. Platforms that monetize only one side of money movement leave revenue on the table.

The opportunity is significant. Edgar, Dunn & Company estimates embedded B2B payments will grow from $4.1 trillion in 2024 to approximately $15.6 trillion by 2030 — nearly a fourfold increase at a 25% CAGR. The pricing decisions you make today will directly shape your margin at that scale.

8. Plan for Compliance from Day One

Compliance is a significant part of any payment platform, not a secondary consideration. PCI DSS (Payment Card Industry Data Security Standard) for card data security, NACHA rules for ACH transactions, KYC/KYB verification for merchant identity, and state-level money transmitter regulations are some of the requirements for handling payments.

The best practice would be to work with an infrastructure partner that handles compliance as a part of the platform itself. Encryption, tokenization, and fraud detection should be part of the backbone of the platform. With the right partner, engineering overheads, risk exposure, and ongoing audit costs could be avoided, which are usually faced by platforms trying to manage PCI scope internally.

Build Your Embedded Payments Strategy with Payabli

Payabli’s unified API consists of Pay In, Pay Out, and Pay Ops, providing vertical SaaS companies with a single integration for acceptance, disbursements, and operations. With white-labeled onboarding, transparent revenue sharing, and no-code components, platforms can go live within weeks rather than quarters.

100+ vertical SaaS platforms and 60,000+ merchants across education, fitness, construction, property management, field service and government are powered by Payabli. Whether you are initially launching payments or replacing a legacy integration, Payabli’s team can help you build a custom payment strategy for your vertical.

Talk to Payabli’s team and see how embedded payments can work for your platform.