Key takeaways

- Financial infrastructure is how vertical SaaS platforms monetize the transaction volume already flowing through their product by owning payment acceptance, accounts payable, and the operations that connect them.

- Most SaaS platforms only earn from the money their merchants collect. Financial infrastructure opens a second revenue channel for the money merchants send, through the same integration.

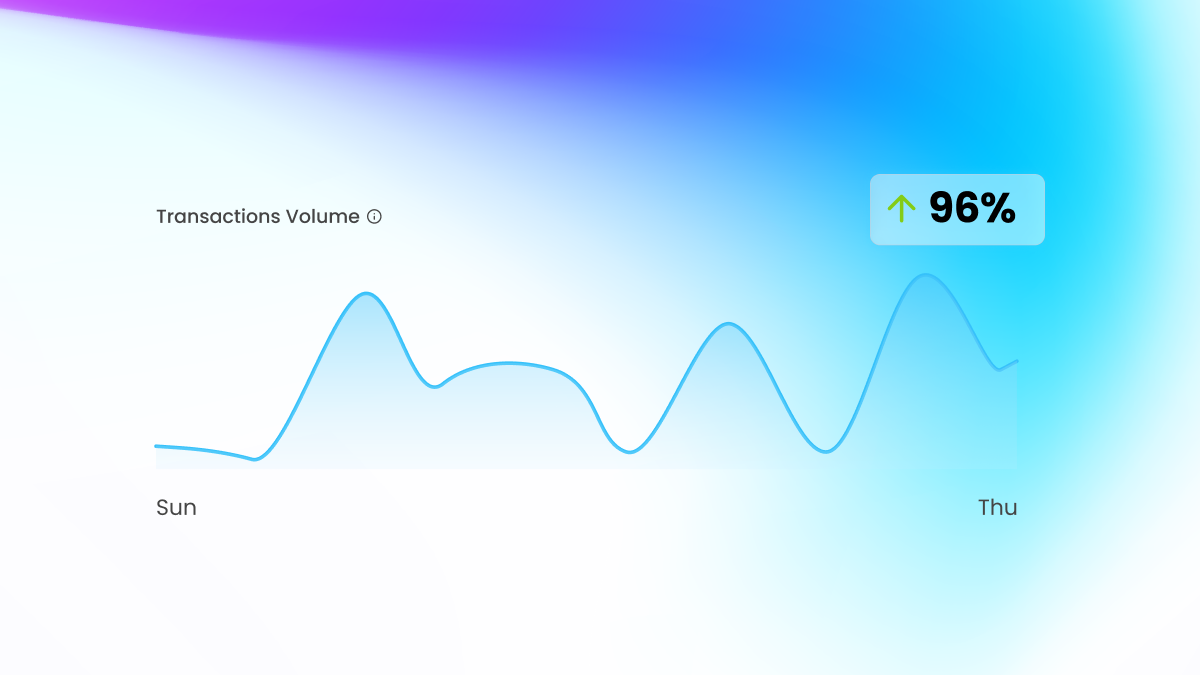

- Fintech-led vertical SaaS companies hold the strongest retention profile of any category, with 96% gross retention versus roughly 90% for other product types.

- The right financial infrastructure strategy starts with auditing, where money already moves through your product, not with picking a vendor.

Subscription revenue only grows when you add new customers. Financial infrastructure revenue grows every time your existing merchants process a transaction. Median SaaS growth rates have settled at 26%, down from 30% two years ago, and net revenue retention across the industry has compressed to 101%. The SaaS platforms pulling ahead are not adding features. They are building a financial layer that earns on every transaction their merchants process.

This blog covers what financial infrastructure means for a SaaS platform, how it generates revenue, and how to build a strategy around it.

What is financial infrastructure for a SaaS platform?

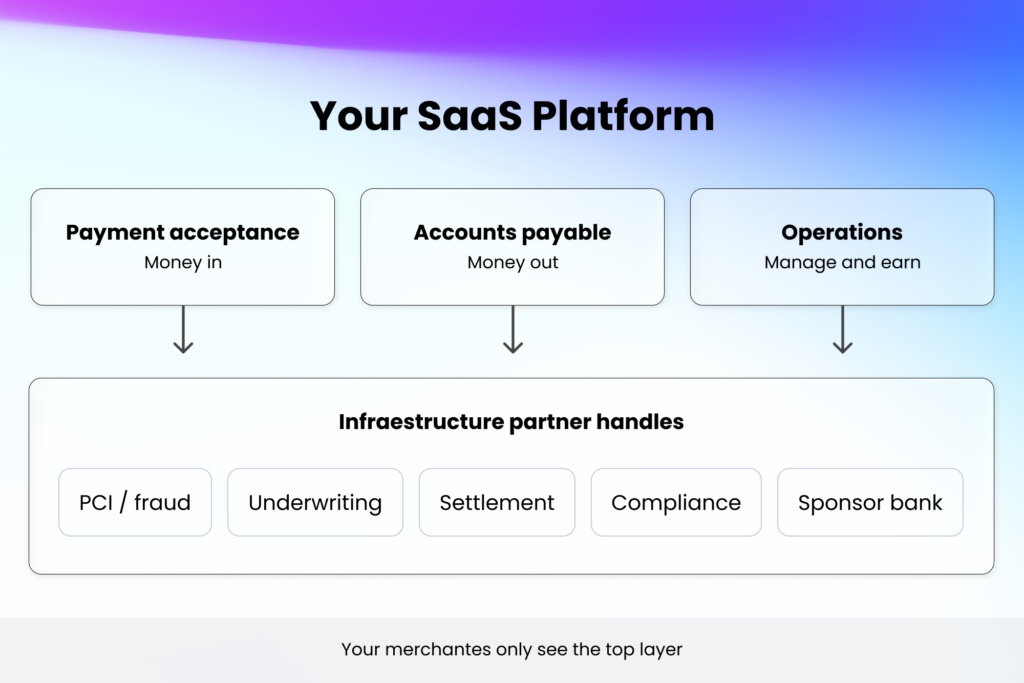

Financial infrastructure is what lets your SaaS platform accept, send, and earn from your merchants’ money. It covers three functions: payment acceptance (Pay In) from your merchants’ customers, accounts payable (Pay Out) to their vendors and partners, and the operational layer (Pay Ops) connecting both, including onboarding, underwriting, risk, billing, and reconciliation.

Financial infrastructure vs. payment processors

A payment processor handles one job: moving money from point A to point B. Your SaaS platform sends a transaction, the processor routes it, and a third party collects the margin.

With financial infrastructure, the economics start to shift. Your platform sets merchant pricing, the infrastructure partner processes through a unified API, and you keep the spread between the two. You also own the transaction data, which means you can optimize pricing by segment and track adoption across your merchant base.

What makes financial infrastructure a revenue layer for SaaS?

Subscription revenue grows when you add customers, while payment revenue through financial infrastructure grows when your existing customers grow, with no upsell and no new contract.

That compounding dynamic is why fintech-led vertical SaaS companies hold the strongest retention profile of any category, with 96% gross retention versus roughly 90% for other product types, according to the benchmark report by Tidemark. The more financial workflows a merchant runs through your SaaS platform, the better their experience, the more revenue you earn, and the harder your product is to replace.

How does financial infrastructure actually generate revenue?

SaaS platforms generate revenue from financial infrastructure on two sides: the money their merchants collect and the money their merchants send. Most platforms only monetize the first.

Transaction spread explained: where SaaS payment margin comes from

Every payment your merchants process through your SaaS platform has an underlying cost. Your platform charges your merchants a rate above that cost. The difference is your margin.

That margin exists on both sides. On the Pay In side, you collect margin on every transaction your merchants collect. On the Pay Out side, when merchants pay vendors through your platform, you earn on each outbound payment too.

In practice, the key variable in SaaS payment margin is not the rate. It is volume. A SaaS platform with 200 merchants processing $300,000 each annually sits on $60 million in volume. That is revenue your subscription model cannot produce without adding new customers.

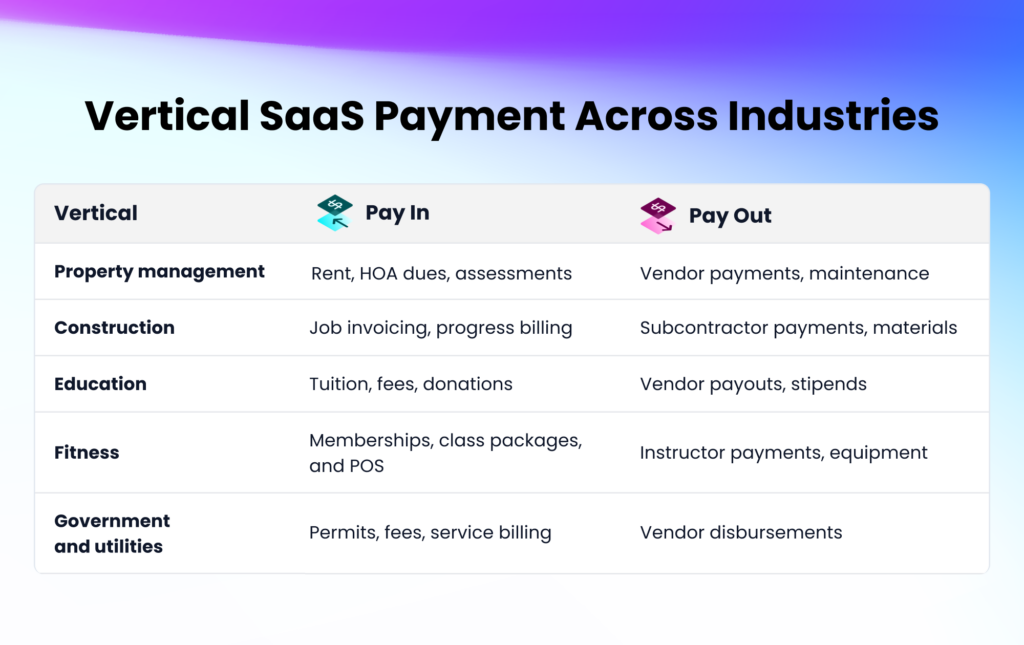

Which vertical SaaS industries earn the most from embedded payments?

In vertical SaaS, the highest-value financial infrastructure opportunities sit in industries where merchants cannot operate without processing payments through the platform. Here are some of the verticals where SaaS platforms generate revenue on both sides:

How do you build a financial infrastructure strategy for SaaS?

Most SaaS platforms pick a vendor before they know what they are monetizing. The sequence below starts with scope, not technology.

Step 1: Audit where money already moves through your product

Before evaluating vendors, define the scope of your financial infrastructure. Map where merchants collect money, where they send it, and where they leave your product to do either. That map determines whether you start with acceptance only or launch with acceptance and accounts payable together.

Step 2: Choose your integration model

There are three primary paths. A hosted solution gets you live in one to two weeks with minimal engineering lift — Payabli manages underwriting, risk, and support while you start generating revenue immediately. Embedded components go deeper, embedding payments natively into your platform in four to six weeks, with the flexibility to take on more operational ownership at your own pace. An API build gives you full control over every touchpoint — custom underwriting, risk, pricing, and merchant lifecycle management — for platforms ready to operate like a full-stack payments business.

What makes Payabli different is that you’re not locked into one path. You can start hosted, layer in embedded components, and graduate to API when you’re ready — without ever needing to re-platform.

Step 3: Set pricing and revenue share that scales with your merchants

Your pricing model shapes your margin at every scale. Payabli gives you full visibility into your cost structure so you can build pricing around your vertical, not a generic blended rate, and set different rates for different merchant segments. Whether you’re running flat rate, tiered pricing, or interchange plus, the right infrastructure gives you the pricing tools and cost transparency to make this practical from day one.

Step 4: Make payments the default

None of this matters if your merchants don’t actually activate. Payments should show up where the work happens, inside the invoice, inside the vendor payout, not behind a settings tab. Set enrollment as the default during onboarding and track merchant activation rate from day one. Activation rate is the percentage of your merchants actively processing through your platform. It belongs next to retention and NRR on your dashboard.

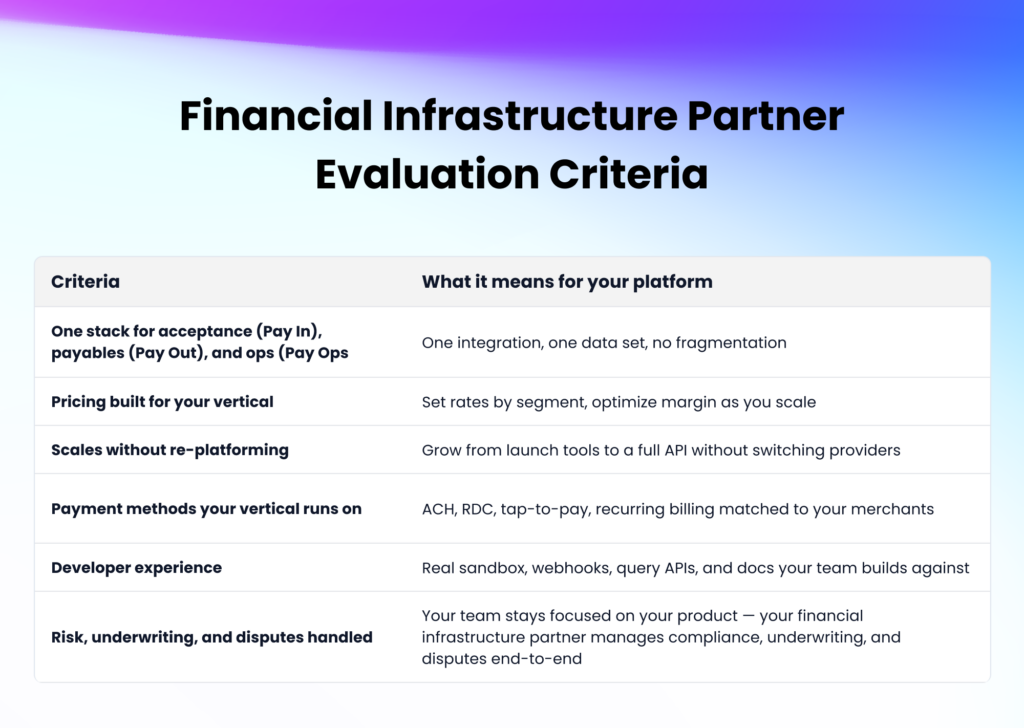

How do you evaluate a financial infrastructure partner for SaaS?

You have the strategy. Now you need a partner who can execute it. Get this wrong, and you rebuild.

How can Payabli help build your SaaS financial infrastructure?

Payabli was built to help vertical SaaS platforms do exactly what this blog describes. Payment acceptance, accounts payable, and payment operations run through a single API, so you do not stitch together three vendors to cover what should be one infrastructure layer.

Beyond the integration, Payabli gives you full visibility into your cost structure, segment-level pricing controls, and interchange optimization guidance so your platform is built to capture margin from day one. Every partner gets a dedicated payments team that knows their vertical and helps shape a go-to-market strategy around payments — not a generic onboarding checklist. The conversation starts with where you are and where you want to go, not with a product pitch.

Request a demo, and we will map the financial infrastructure opportunity for your platform.